China's LPR sounds the alarm

An important event took place today, but it did not receive the attention it deserved. The People’s Bank of China (PBoC) decided to keep its key loan prime rates unchanged, maintaining the 1-year LPR at 3.1% and the 5-year LPR at 3.6%. Under normal circumstances, such a move could be seen as a signal of economic resilience. However, we take a different view: this decision is not a sign of strength but rather a symptom of the banking sector’s struggles. As I discussed in a previous post, banks are already operating with thin net interest margins (NIMs), meaning any further rate cuts would erode their profitability, limit their ability to absorb growing bad debts, and further constrain lending.

In China’s credit market, most lending under the LPR framework is directed at large state-owned enterprises and financially strong firms (this rate represents the interest level at which banks lend to these entities under near risk-free -ish conditions), which already enjoy preferential rates. Lowering rates further would do little to stimulate broader credit growth, as banks remain hesitant to extend credit beyond their safest customers. The reluctance of banks to take on additional risk demonstrates that monetary easing alone is insufficient to drive economic expansion.

The problem facing China’s banking sector is closely tied to the ongoing property crisis threatening to the financial stability itself. While authorities have attempted to downplay risks, a closer look at the numbers reveals a system overwhelmed by rising nonperforming loans (NPLs), squeezed liquidity, and an increasingly fragile credit environment.

More specifically, housing investment in China has continued its contraction in year-over-year property investment. Although there has been a slight improvement, it remains well below the levels seen in previous years. In February 2025, the contraction stood at -9.8%, a slight improvement from -10.6% in December 2024. However, the truly alarming aspect is that year-over-year property investment has not been positive since March 2022, when it briefly reached 0.7%.

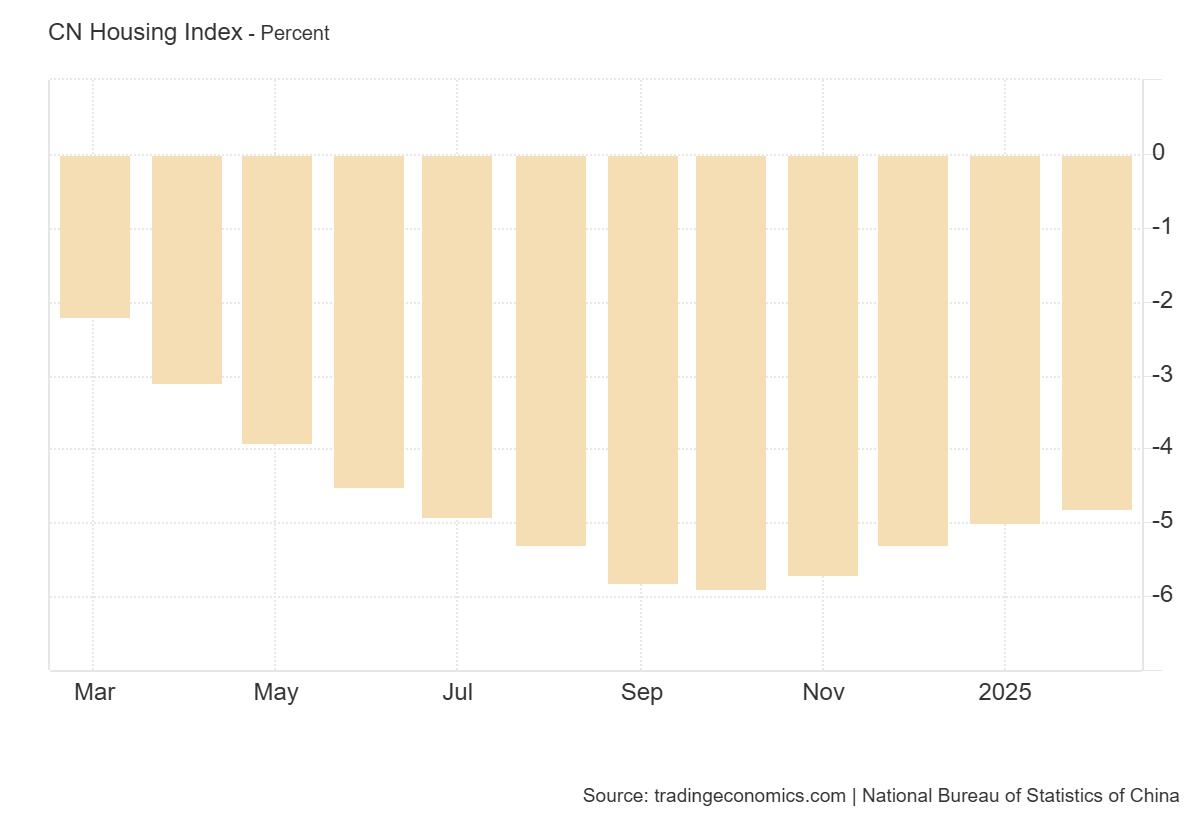

Moreover, new built house prices (year-over-year) contracted by nearly 10% in the first two months of the year (signaling prolonged distress in the real estate sector).

With demand stagnating, major property developers continue to face liquidity crises, leading to further distress in the financial system.

Estimates initially suggested that property-related loans constituted around 40% of Chinese bank assets, but even with a decline in this share, real estate exposure remains a key risk. The property sector has long been a cornerstone of China’s economy, with banks heavily involved in mortgage lending and developer financing. The ongoing slump, however, has led to a sharp rise in bad debts.

Rising Nonperforming Loans and Liquidity Pressures

S&P Global estimates that China’s commercial banking sector’s NPL ratio will rise to 5.7% by 2026, up from an estimated 5.6% in 2023. While the Chinese government’s official NPL ratio stood at 1.6% in 2023 - the lowest since 2014 - the discrepancy between official data and industry projections raises questions about the accuracy of government figures.

For property development loans, the situation is even worse. As Barrons specified, the NPL ratio for such loans is expected to peak at 6.4% by 2025, more than double the 2.79% median NPL ratio for property-related loans among China’s top 18 banks as of mid-2023. The same for non-performing assets (NPAs) ratio, that is expected to reach 5.5%, up from 5%, which represented the previous estimates. The country’s “big four” state-owned banks reported an average bad loan ratio of 5.2% for property-related lending in mid-2023, a slight decline from 5.5% at the end of 2022. However, smaller banks, particularly those in rural and small-city areas, lack the capital buffers of their larger counterparts, making them even more vulnerable to financial shocks.

To address systemic fragility, Chinese regulators have resorted to forced consolidations. In June 2024 alone, 40 small banks disappeared through mergers, while Henan province announced plans to consolidate 25 banking institutions into a single provincial-level rural commercial bank. Such moves highlight the sector’s weakness and the lack of proper resolution mechanisms for failing banks. According to S&P Global, it may take up to five years to substantially clean up high-risk rural financial institutions.

The Road Ahead

The outlook for China’s banking sector remains precarious. The decision to hold the LPR steady highlights the difficult position policymakers are in: lowering rates would only exacerbate the financial strain on banks, while maintaining them reflects the severity of existing economic weaknesses. While authorities have focused on managing risks through bank mergers and liquidity interventions, the underlying structural issues persist. The property market downturn continues to weigh on financial institutions, and rising NPLs pose a serious threat to banking stability. With economic conditions deteriorating, the inability of banks to extend credit beyond safe borrowers suggests that China’s financial system is far from stable, despite official assurances to the contrary.

And given the way things are looking, not even the financial bazooka deployed by Chinese policymakers can significantly improve the situation. Tick-tock…

An excellent recap Alex. I cannot help but look at Japan and the lost decade(s) that were a result of the collapse of the property bubble there in the late 1980's and think that the idea China's banks will recover any time within the next 10 years, let alone by the end of the decade, are propaganda perpetrated by the CCP to demonstrate the alleged strength in their economy. As well, I cannot help but look at the fact that the Chinese people were led to believe that property investment was the key to their own savings and retirement process, and now so many are under water that any idea the Chinese consumer will increase spending significantly just because the government is allegedly going to pump some money into the economy is completely incorrect.