Dark clouds are gathering... all over the Euro Area

Here we are! The latest data on labor costs and inflation in the Euro Area and EU paints a picture of an economy on the edge of a downturn - one that hasn’t yet officially fallen into recession but is undoubtedly feeling the weight of a prolonged economic struggle. There are several signs pointing us in that direction.

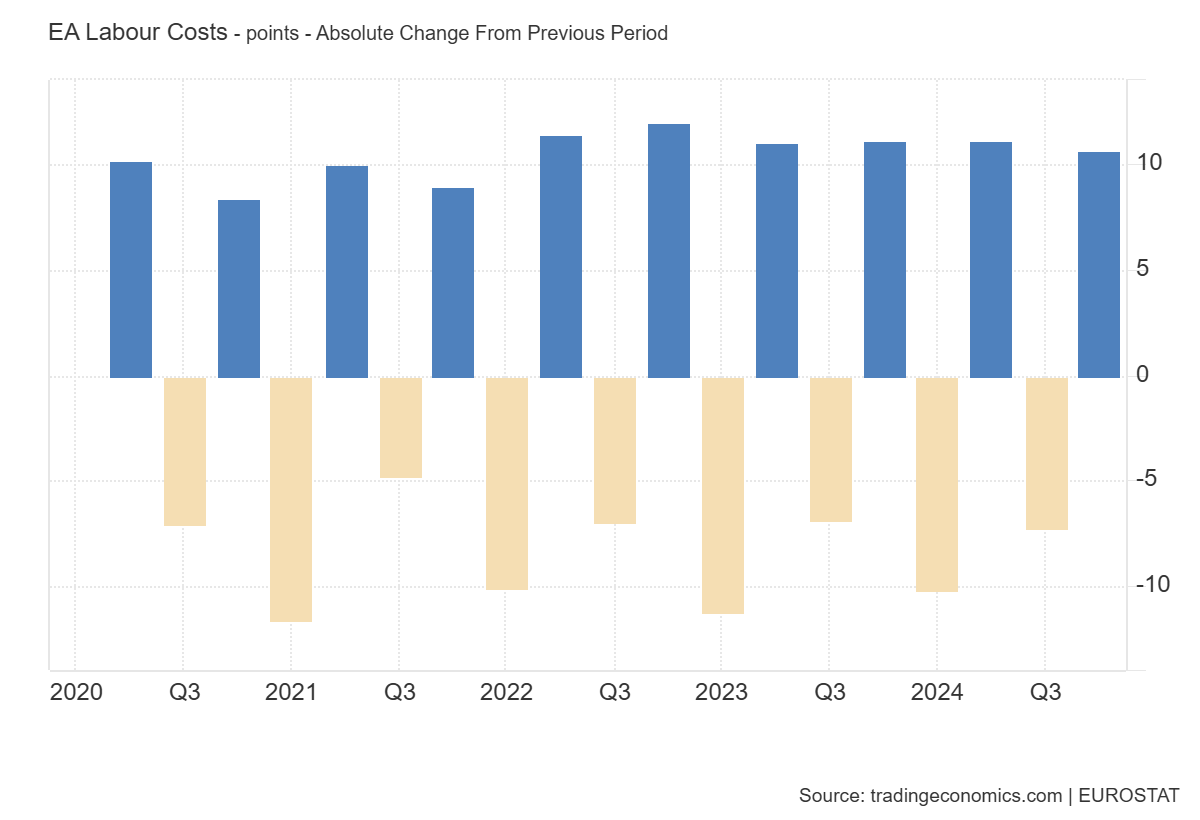

For instance, hourly labor costs in the Euro Area rose by just 3.7% in Q4 2024 compared to the previous year, marking the lowest increase since Q3 2023. In terms of points, the situation looks even worse, as it’s the lowest since Q4 2021, essentially during the pandemic crisis - 10.7 in Q4 2024 compared to 9 points in Q4 2021. This slowdown is likely a result of diminishing fiscal and monetary stimuli (which had artificially propped up the labor market but failed to address structural issues, as shown once again).

Moreover, wage growth doesn’t paint a much brighter picture. Although wages increased by 4.1%, the non-wage component grew more modestly at 2.6%, suggesting that companies are trying to contain additional costs amid a less-than-optimistic economic outlook. However, even that 4.1% is on a steady decline, reaching its lowest point since Q4 2023 when it was at 3.7%.

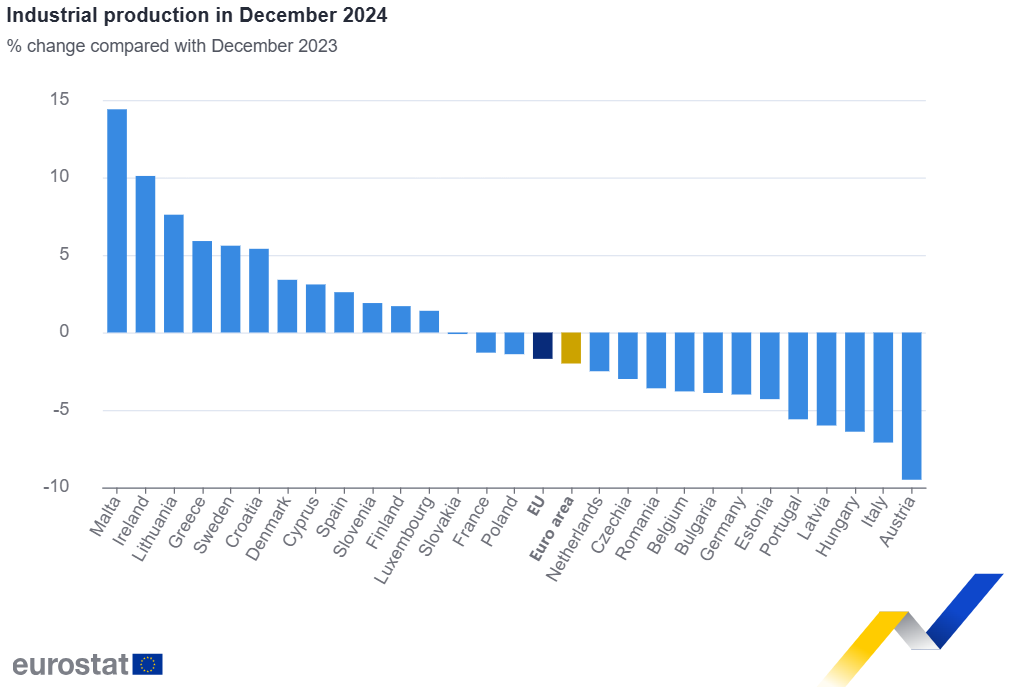

Looking deeper into different sectors, the services industry saw the smallest rise in labor costs (3.7%), followed by construction (4%) and industry (4.3%). Wage growth across these sectors has slowed considerably. In construction, wages grew 4.3%, down from 4.8% in the previous quarter, and in services, wage growth fell from 4.3% to 4%. The industrial sector, in contrast, saw a slight acceleration in wage growth from 4.4% to 4.7%. Yet, this slight uptick does little to offset the broader trend of stagnation across the economy, especially since this acceleration is not proportional to industrial production growth. On the contrary, industrial production in the EU, as well as in the Euro Area, is negative year-over-year.

Another factor is the slowing wage growth. This comes at a time when productivity is also weakening. In Q4 2024, productivity in the Euro Area fell to 103.30 points, down from 103.69 points in the previous quarter, continuing a pattern of decline from the peak seen in 2020. This drop suggests that the economic momentum many hoped for post-pandemic remains elusive. As businesses grapple with stagnating demand, particularly in key sectors like manufacturing, they are finding it increasingly difficult to balance labor costs with falling productivity.

Though the economy hasn’t officially entered a recession, it’s hard to ignore the familiar signs: weak demand, slowing wages, and shrinking productivity. Companies are adjusting to these conditions by holding back on hiring or even reducing labor costs where they can. Meanwhile, the once-strong post-pandemic recovery phase seems to have fizzled out, leaving a sense of stagnation hanging over the region.

Last but not least, inflation figures are also showing signs of slowing, with the annual inflation rate for the Euro Area dropping slightly to 2.3% in February 2025 from 2.5% in January. But let’s not be fooled by this reduction. Much of this decline is a result of base effects and the easing of energy prices, rather than a sustained improvement in the underlying economic conditions. Services remain the primary driver of inflation, but the overall pressure from energy and industrial goods has lessened.

While inflation may be slowing, the broader economic conditions in the Euro Area point to a period of prolonged sluggishness. The labor market is adjusting to a new reality without pandemic-era support, and businesses are finding it increasingly difficult to thrive in this environment. While we’re not technically in a recession, the economic trajectory is far from robust, leaving many to wonder how long this slow-motion stagnation can persist without tipping into something worse.