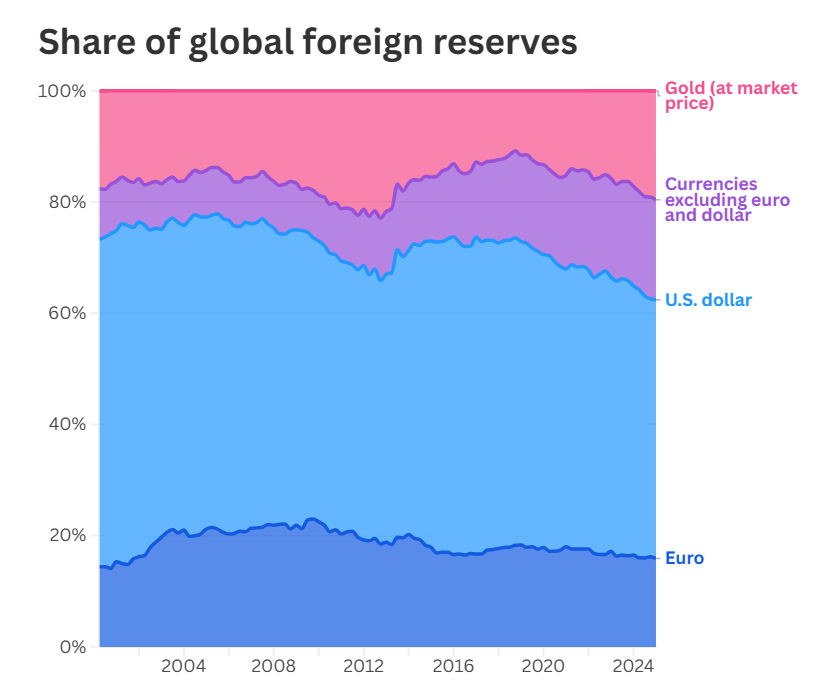

The international monetary system is undergoing (yet another) significant transformation. According to the European Central Bank’s (ECB) latest report, gold has now overtaken the euro as the world’s second-largest reserve asset held by central banks, trailing only the US dollar. Gold now accounts for 20% of global official reserves - up from around 10% just a decade ago - whereas the euro has slipped to 16%. This shift shows both the growing limitations of the euro as a global reserve currency (as it’s going to be discussed below) and the strategic recalibration among emerging economies increasingly skeptical of fiat-based reserve structures.

Source: CNBC

The surge in gold’s share is driven by two key dynamics: persistent central bank purchases - led by countries such as China, India, Turkey, and Poland - and a meteoric price rally, with bullion climbing over 30% last year and a further 27% year-to-date, reaching a historic $3,500 per troy ounce. Central banks now hold nearly as much gold as they did during the height of the Bretton Woods system in the mid-1960s, when the dollar’s convertibility into gold anchored the global monetary order.

But what lies beneath this preference for bullion?

For one, gold is a non-liability asset. It carries no counterparty risk and no exposure to political pressure, unlike reserve holdings in major currencies. In a world marked by growing geopolitical fragmentation, central banks - especially in emerging markets - view gold as both a hedge against sanctions and an insurance policy against the erosion of existing currency hierarchies. Survey data referenced by the ECB points to rising concerns among these countries about over-reliance on the dollar or the euro, particularly in light of recent US-led financial sanctions and the EU's fragmented fiscal architecture.

Source: European Central Bank

This brings us to the euro’s declining role. Despite two decades of monetary integration, the eurozone has failed to construct a robust foundation for the euro as a safe, global reserve currency. One key factor is that the euro was never designed with internationalisation as a core objective. From the outset, the Eurosystem explicitly stated that it would neither promote nor hinder the euro’s international role, asserting that such a development would be market-driven. Starting from such a position makes it inherently difficult to build momentum toward internationalisation, especially in a short time frame. In theory, this process began only recently, around the time of the Covid-19 pandemic, when the ECB adopted elements of the Federal Reserve’s approach and began establishing euro swap lines with non-euro area central banks. Finally, in January 2024, the ECB adjusted its framework for providing euro liquidity by introducing a unified permanent framework called the Eurosystem Repo Facility for Central Banks (EUREP), alongside the existing swap lines with non-euro area central banks (in addition to the standing arrangements established after the 2007 global financial crisis).

For those unfamiliar, a swap line refers to an arrangement in which one central bank provides liquidity in its own currency to another, typically in exchange for that second central bank’s currency or eligible collateral. And while, in principle, swap lines can promote the international use of a currency, the ECB, in my view, made a strategic misstep.

Unlike the Federal Reserve, the ECB aims to avoid unhedged currency exposures in the countries receiving euro liquidity and to limit the extent of financial “euroisation”. This reflects a fundamentally different set of incentives compared to the Fed, for instance. Moreover, it has already been argued that these swap lines are structured in a way that encourages a return to market-based arrangements, offering only short-term funding with a maximum tenor of a few months to ensure they address only temporary liquidity needs. In plain terms: “we’re willing to provide you with euros, but not so you can do whatever you want with them, not to expand your euro positions, not to support you directly or indirectly in carry trade transactions, and certainly not to help you further develop the the offshore euro market”. In this direction, the ECB has committed to adjusting the pricing applied to these lines in order to discourage borrowing, depending on its monetary policy objectives.

Not even the ECB’s new repo facility (part of EUREP) meaningfully alters the structural equation. Through this repo facility, ECB aims to provide euros against EUR-denominated collateral, already accepted within its collateral framework. Even though this is good news, the ECB continues to act in a discretionary manner. For instance, all repo lines have a predefined end date, and the approval and extension of such a line depends on an assessment of a monetary policy case. In other words, these facilities are primarily offered to the euro area’s strategic partners and come with a cost that makes them suitable only during periods of economic stress or when monetary policy transmission might be disrupted. This means that repo lines are terminated once conditions normalize. Under these circumstances, the ECB's repo facilities are not explicitly aimed at increasing the international use of the euro. If that were the case, they would not be priced in a way that only makes sense in crisis conditions. Instead, the true purpose of these lines is to prevent disorderly sales of euro-denominated financial instruments abroad, the upward pressure on euro money markets and to safeguard the effectiveness of the ECB’s monetary policy. This is all the more important given the ECB's clear preference for using repo transactions as part of the EUREP framework, a decision driven by its aim to avoid “loading” its balance sheet with foreign currencies that carry financial risks (as would be the case with swap lines).

Equally important, a major structural obstacle to the internationalisation of the euro is the chronic shortage of euro-denominated safe assets. Unlike the United States, where the Treasury market supplies roughly $21 trillion in freely available sovereign debt not held by the Federal Reserve, the euro area offers just €4 trillion in highly rated, marketable government securities not held by the ECB. This severely limits the euro’s usability for collateralized transactions, including repo markets, and dampens its appeal to foreign reserve managers.

The institutional roots of this problem run deep. EU fiscal rules discourage expansive sovereign debt issuance, and supranational issuance - such as through the Recovery and Resilience Facility (RRF) - remains politically constrained and temporary. As I discussed just a few days ago, EU Bonds - one of the few instruments with the potential to fill this gap - will no longer be issued starting next year. This development further weakens the euro’s capacity to compete globally as a reserve currency, as the supply of high-quality, marketable sovereign debt remains fragmented and insufficient across the euro area. Compounding this, the ECB has historically refused to backstop euro-area sovereign debt in a consistent, unconditional way. Its 2005 decision to condition collateral eligibility on credit ratings entrenched intra-euro area spreads and signaled an unwillingness to support euro-denominated debt with the same resolve that the Federal Reserve shows toward Treasuries.

This structural deficiency in safe asset supply impedes euro internationalisation. Safe assets are essential not just for investor confidence, but for enabling offshore euro liquidity creation, much like how US Treasuries underpin the global shadow banking system through repos and other instruments. Without a deep and unified pool of euro-denominated safe assets, the euro lacks the infrastructural depth needed to rival the dollar, no matter how sound the ECB’s monetary policy.

In this context, gold’s rise is a symptom of broader disillusionment. It reflects not only fears about fiat currency debasement and geopolitical volatility but also a pragmatic assessment: when institutional constraints prevent the euro from stepping up, gold offers stability without strings attached.

If the EU wants to reverse this trend, it must confront its longstanding reluctance to federalize fiscal risk and build a truly pan-European safe asset. Without this, the euro’s global role will continue to stagnate while bullion’s quiet ascent continues.