Good news in the Eurozone lending data? Hold your horses

The recent data on Eurozone bank lending suggests that bank credit has increased. In theory, this should be a good thing, meaning the economy is starting to recover. The thing is… not really. As usual, it's a false alarm. While it can be argued (although I wouldn’t make this argument) that the European Central Bank’s (ECB) easing measures have contributed to a slight acceleration in credit growth, I would add that the broader lending environment remains subdued.

Lending to both households and non-financial corporations (NFCs) rose marginally in February, but the increase - 1.5% for households and 2.2% for businesses - remains well below pre-pandemic levels. This modest uptick does little to suggest a robust expansion in private investment, and instead, the data points to a financial system still operating in a defensive mode.

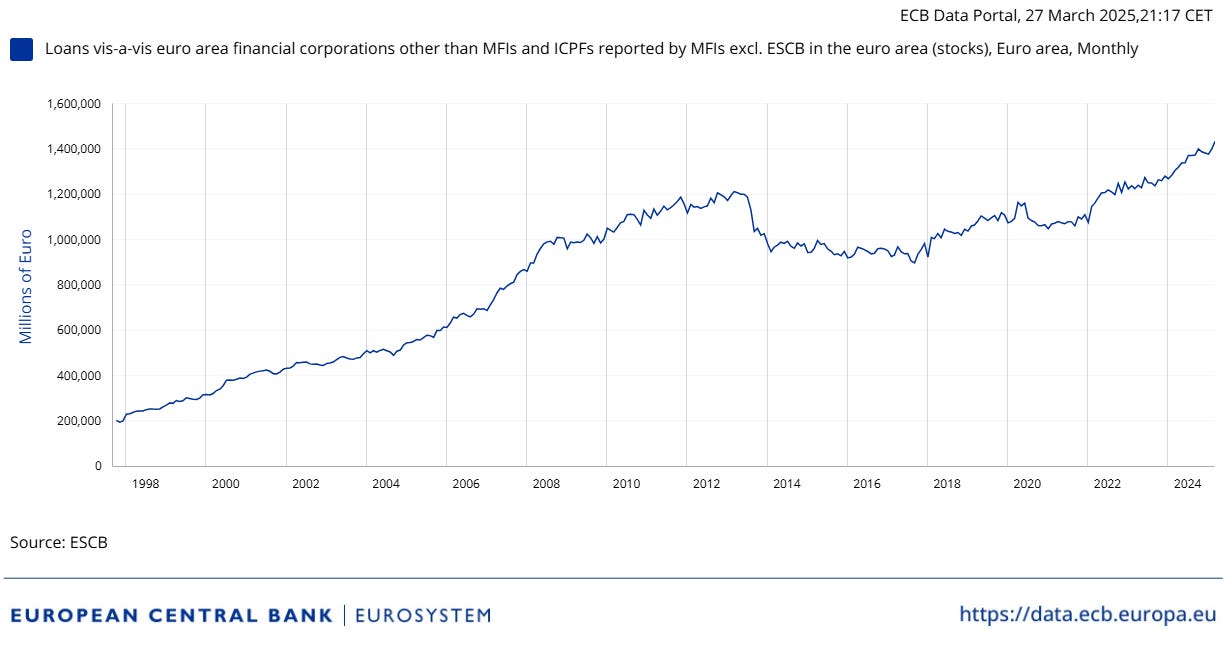

Why do I say banks are acting “defensively”? It is important to examine the direction of these loans. For instance, a closer examination of credit distribution reveals that the bulk of new lending has flowed to non-MFI (monetary financial institution) financials, such as investment funds and Special Purpose Vehicles (SPVs), among others, rather than to households and firms. This is essentially related to portfolio adjustments—essentially, a way for banks to reconfigure their risk profile.

This implies that banks remain reluctant to extend credit to the real economy, preferring instead to allocate funds to entities that function within the financial sector itself. This pattern suggests a continuation of balance sheet conservatism among banks, where liquidity is preserved within the financial system rather than fueling productive economic activity. And this should not come as a shock. In the Bank Lending Survey from January, banks reported tightened credit standards for consumer credit and other lending to households. The next survey will come next month, but I don’t expect things to change fundamentally. This again points to the constant effort by banks to reduce the risks they take on in their balance sheets. Even for businesses, the same net tightening was announced, following the unchanged credit standards seen in the third quarter of 2024. It was linked to the higher perceived risks related to the economic outlook, the industry- and firm-specific situation, and banks’ lower risk tolerance.

In parallel, another key trend highlights this defensive posture: the substantial increase in government bond holdings, which is hovering around an all-time high. Okay, the explanation could also be linked to the high levels of government debt in recent years, especially post-pandemic, but the figures remain relatively elevated, particularly after 2023.

Thus, rather than deploying capital into higher-risk loans, banks appear to be shifting toward the relative safety of sovereign debt. This signals caution in the face of lingering economic uncertainties and suggests that financial institutions still perceive risks in lending to the private sector. The result is a lending environment where credit is available but not necessarily reaching the areas most essential for broad-based economic growth.

The broader monetary aggregates further illustrate the caution in the Eurozone. The annual growth rate of M3 rose to 4.0% in February, indicating a gradual increase in liquidity. However, its composition is telling: M1, which includes currency in circulation and overnight deposits, grew at 3.5%, suggesting that liquidity is increasing but not necessarily being deployed into long-term investments. Meanwhile, another important factor is represented by M3-M2, which stands for marketable instruments. The sharp increase in M3-M2 (19.8% annual growth) indicates a preference for short-term, liquid financial assets over traditional lending channels. This is likely driven by expectations of further monetary easing (which, under these conditions, reflects negative expectations about the Eurozone economy, as I have argued here), rather than stronger economic momentum. Moreover, this growth in liquid financial instruments is a result of economic uncertainty and, consequently, a decrease in risk appetite.

Ultimately, the Eurozone’s credit growth appears to have bottomed out in late 2024, but the current trajectory suggests only a mild expansion. While lending is no longer contracting, the underlying trends reflect a cautious financial system that remains hesitant to fully re-engage with the real economy.

In this context, monetary policy alone may struggle to generate a significant acceleration in economic activity (as expected), leaving fiscal interventions as the primary catalyst for growth in the near term (as mainstream economists would say). However, even this catalyst works only in theory and rarely in practice...