Back to the (UST) futures

What are treasury futures? Briefly, a Treasury futures contract is an agreement to transact in the future at a price agreed upon today. Why is it relevant? Since 2020, mutual funds have become increasingly reliant on Treasury futures to manage interest rate risk, access leverage, and optimize their portfolio returns. This trend marks a significant structural shift in how fixed-income mutual funds obtain US Treasury exposure, away from cash securities and repo borrowing, and toward derivatives markets.

Source: Federal Reserve

As of June 2023, mutual funds accounted for over half (53%) of all long Treasury futures positions held by asset managers, amounting to roughly $579 billion in notional value. This represented about 31% of all long open interest in the Treasury futures market. Between mid-2021 and mid-2023, mutual funds were responsible for 62% of the overall increase in open interest in these contracts. During that time, their notional exposure to Treasury futures surged by 65%.

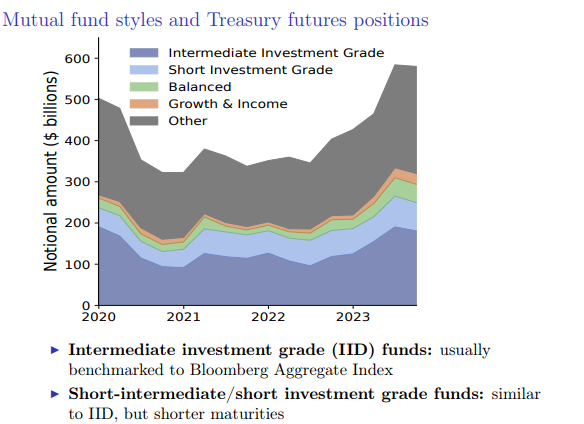

This increased use of futures has come at the expense of direct holdings of Treasury securities. While the Bloomberg US Aggregate Index - the benchmark for many of these funds - has steadily increased its Treasury weight (from 35% in 2011 to nearly 45% in 2023), mutual funds have not mirrored that growth with equivalent cash holdings (see the figure below, these is a slump at the end of 2023). Instead, they have used Treasury futures to replicate the index’s duration exposure while allocating more capital to higher-yielding assets such as corporate bonds, MBS, collateralized loan obligations (CLOs) and even equities. Why? Because it ensures a greater return on investment. As such, the mutual funds’ usage of Treasury futures is today associated with greater risk taking, suggesting that mutual funds use the embedded leverage in futures to increase exposures to riskier assets.

Source: Federal Reserve

Thus, we can distinguish between two types of strategies. The first, known as “reaching for yield”, has just been discussed. The second, often referred to as “reaching for duration”, reflects a deeper structural tension. On the one hand, mutual funds must match the duration profile of their benchmark index (as the Bloomberg US Aggregate Index). On the other, they face pressure to enhance returns in a low-yield environment. Cash Treasuries, especially off-the-run securities, offer safety and duration but at a cost: lower yield, reduced liquidity, and unfavorable accounting treatment under certain regulatory regimes.

Treasury futures help resolve this tradeoff. They allow funds to synthetically extend portfolio duration using less capital and less balance sheet. This embedded leverage allows funds to maintain interest rate exposure with fewer cash Treasuries, freeing up capital for riskier assets with better return profiles. SEC filings confirm that as funds increase their long futures positions, they simultaneously reduce Treasury holdings and increase allocations to MBS and equities.

In other words, when mutual funds rotate into higher-yielding assets like MBS or even CLS, they remain benchmarked to indices like the Bloomberg US Aggregate, which carry significant Treasury exposure. Selling Treasury securities lowers portfolio duration, creating tracking error (meaning their portfolio no longer mirrors the benchmark in terms of interest rate exposure). If rates fall, the fund underperforms the benchmark. To fix this, funds buy Treasury futures. These contracts offer cheap exposure to interest rate risk. By going long futures, mutual funds can restore portfolio duration (without holding the bonds themselves) and still being active in higher yield-generating assets.

But why futures over repo?

In theory, funds could obtain similar leveraged exposure to Treasuries through the repo market, borrowing cash against securities to increase portfolio size. But in practice, this channel is constrained. Regulatory limits (specially SLR, as we discussed here or here), interest expenses, and impacts on reported fund expenses make repo a less attractive option.

Indeed, among mutual funds reporting on SEC Form N-PORT, 84% use only futures for Treasury exposure, 12% use both futures and repo, and just 4% rely exclusively on repo. The simplicity and efficiency of futures make them particularly attractive to fund managers under pressure to deliver performance within regulatory and liquidity constraints.

The preference for futures is also driven by liquidity and execution advantages. Treasury futures are deep, standardized, and easily adjusted, ideal for funds facing volatile investor flows. Modifying interest rate exposure via futures is faster and less costly than transacting in cash Treasuries, particularly in periods of market stress or illiquidity.

Moreover, there is also a cost factor. For instance, futures contracts are centrally cleared and require only margin posting (but also variation margins), not full cash outlay or financing via repo, making them more capital-efficient.

Source: Federal Reserve

However, this trend is not without systemic implications. Mutual funds using Treasury futures tend to exhibit higher risk-taking behavior, greater cash holdings, and more volatile investor flows. Their dependence on leveraged futures exposes them to basis risk, margin calls, and dislocations in derivatives markets (2nd of April anyone?).

As such, liquidity no longer flows through the clean pipes of traditional intermediation. The old system - dominated by primary dealers warehousing bonds on their balance sheets - has given way to a more precarious arrangement between two types of institutions: mutual funds and hedge funds.

How does it work? Mutual funds, especially those managing pensions or benchmark-driven portfolios, want exposure to US government bonds. But in a world of tight cash management, they increasingly prefer Treasury futures over outright bonds. These contracts offer synthetic duration - interest rate exposure without the capital commitment. They’re simple, liquid, and don’t clog up the balance sheet.

On the other side of that futures trade stands the hedge fund. It doesn't want long-duration exposure. What it wants is a pricing mismatch or a basis. So it sells the futures contract the mutual fund is buying and simultaneously buys the underlying cash Treasury bond. To do that, the hedge fund taps the repo market, borrowing against the very bonds it’s purchasing. This is the essence of the cash-futures basis trade: short the futures, long the bond, profit from the spread. More about this topic here, an important phenomenon that was linked to the turmoil in April 2025.

Treasury futures are no longer just simple derivatives, they’ve become an integral part of how the US Treasury market functions. Naturally, this shift carries a range of implications, both positive and negative, and each deserves to be examined in turn. But what truly matters is that the underlying structure of the Treasury market has changed. And it’s my job - our job - to explain exactly how. Until next time!