How special are you?

A short USTs-Bund story

A recent analysis published by the European Stability Mechanism argues that increases in US Treasury supply spill over into German Bund yields and that these spillovers have weakened as Treasuries have become “less special”. The paper estimates that a one percentage point increase in Treasury supply relative to GDP raises Bund yields by approximately 10-15 basis points, while a declining Treasury convenience premium reduces the strength of this transmission mechanism.

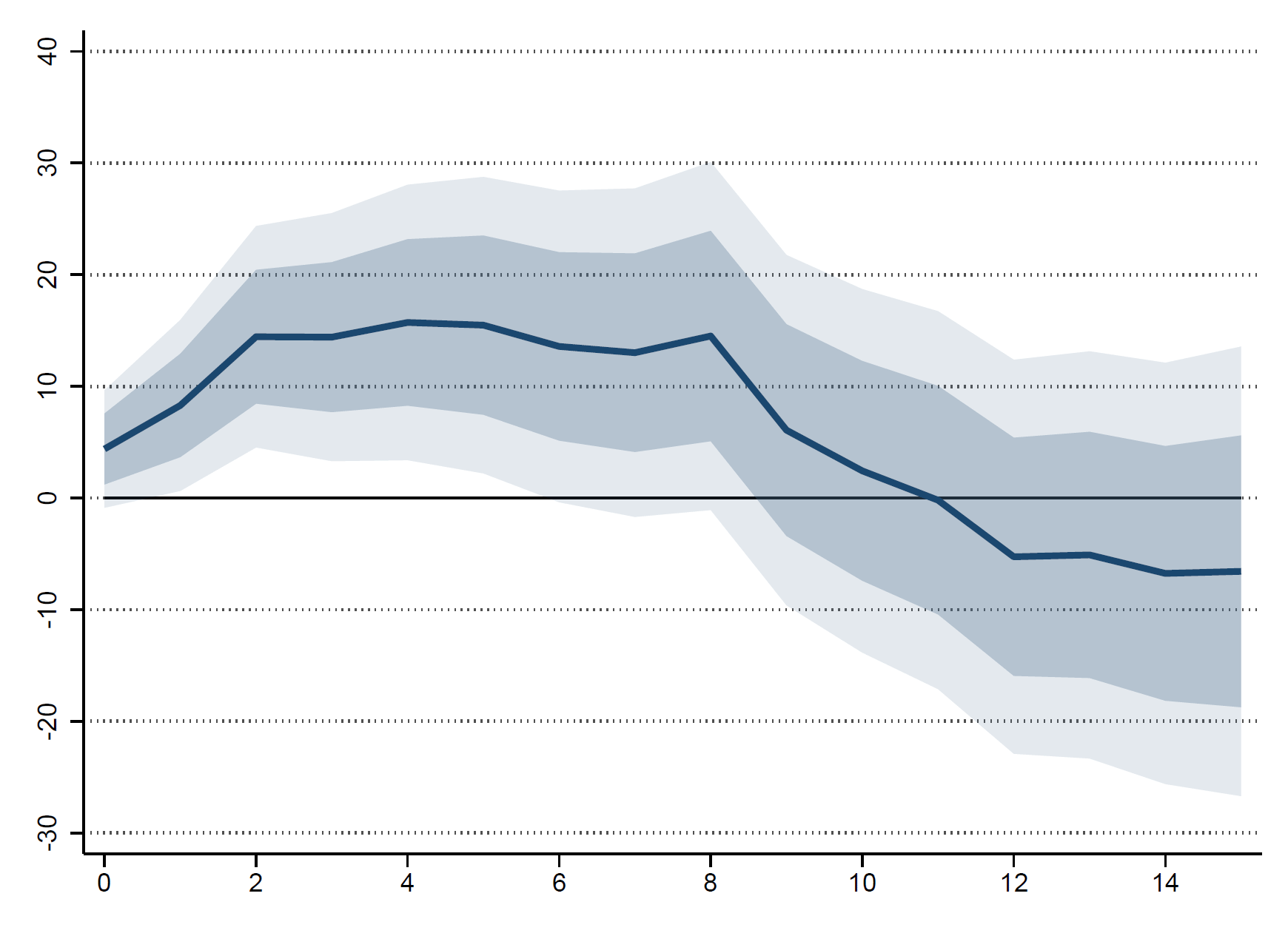

In the figure below we can see the Bund response to USTs supply shock (in bps):

Source: European Stability Mechanism

The empirical finding is both interesting and plausible. Financial markets remain highly integrated, and sovereign bond markets exhibit substantial co-movement. What deserves closer scrutiny, however, is the interpretation of the mechanism. The ESM framework implicitly treats Treasuries and Bunds primarily as competing safe assets within a global portfolio allocation problem. Yet modern sovereign bond markets operate through collateral and funding channels that are difficult to reconcile with a pure portfolio balance framework. Moreover, the notion that Treasuries have become “less special” immediately raises a deeper question: special in what sense?

The literature on convenience yields traditionally interprets specialness as investors’ willingness to accept lower yields on safe assets because they provide liquidity services. The classic work of Ricardo Caballero and Emmanuel Farhi links these premia to global shortages of safe assets and elevated demand for liquidity. Similarly, research from the Federal Reserve Board emphasizes that Treasury convenience yields reflect their role as exceptionally liquid instruments that can satisfy precautionary demand during periods of uncertainty.

However, the post-2008 financial system fundamentally altered the meaning of liquidity. A Treasury security is no longer merely a safe asset. It is also repo collateral, margin collateral, maybe a high-quality liquid asset (HQLA) under Basel regulations. From this perspective, convenience yields and collateral values are not identical concepts. The ESM paper largely interprets declining convenience yields as evidence that Treasuries are losing some of their unique attractiveness relative to Bunds. Yet an alternative interpretation is that the observed decline reflects changes in dealer balance sheet economics.

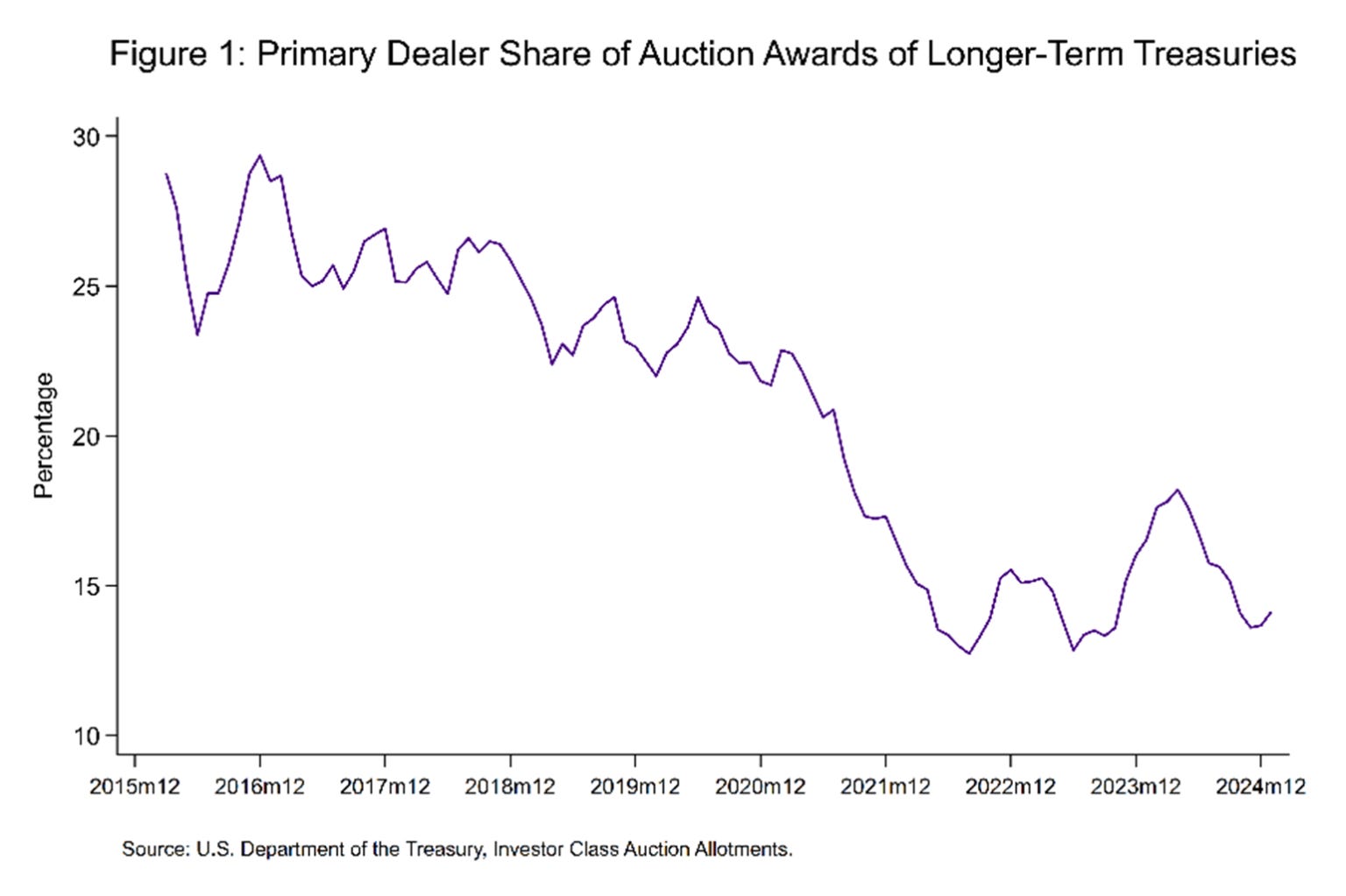

This distinction matters because the Treasury market has undergone profound structural transformations since the GFC of 2007-9. We heard about so many (complex) regulations, Supplementary leverage ratios, GSIB surcharges, liquidity coverage requirements, enhanced stress-testing frameworks, just to name a few. And these regulations have fundamentally altered how dealers absorb sovereign issuance. Research from the Bank Policy Institute (BPI) consistently highlights that post-crisis regulation has reduced dealer balance sheet elasticity, increasing the sensitivity of Treasury market functioning to large issuance cycles.

Source: Bank Policy Institute

Under such conditions, Treasury supply shocks are no longer transmitted exclusively through investor portfolios. They also (or mostly) operate through dealer balance sheets. The September 2019 repo disruption provides a useful example. At the time, aggregate reserves remained historically elevated relative to pre-crisis norms. Yet funding markets experienced severe stress because dealer balance sheets could not expand sufficiently to absorb collateral flows. The resulting spike in repo rates had little to do with investor perceptions of Treasury safety and much more to do with intermediation constraints. In previous posts (for example here or here) I’ve shown that balance sheet constraints were central drivers of the episode.

The same lesson emerged during March 2020. The Treasury market experienced one of the most severe liquidity disruptions in its modern history despite a global flight toward safety. Investors were attempting to sell Treasuries not because they doubted Treasury creditworthiness but because they needed liquidity. Dealer balance sheets rapidly became constrained, producing severe market dysfunction. Research from the BIS demonstrates that Treasury market stress during the pandemic reflected balance sheet capacity limitations as much as changes in investor demand.

These episodes complicate the ESM interpretation. If Treasury supply spillovers increasingly depend on dealer intermediation capacity, then a reduction in observed spillovers may not indicate that Treasuries are becoming less special. Instead, it may indicate that the transmission mechanism itself has shifted from portfolio allocation toward balance sheet management. The issue becomes even more complicated once reserves enter the discussion. The ESM analysis treats Treasury supply largely as an independent variable affecting sovereign yields. Yet from a monetary perspective, Treasury issuance cannot be separated from reserve dynamics. Treasury issuance alters the composition of private sector balance sheets and affects money market conditions through its interaction with the Federal Reserve’s balance sheet.

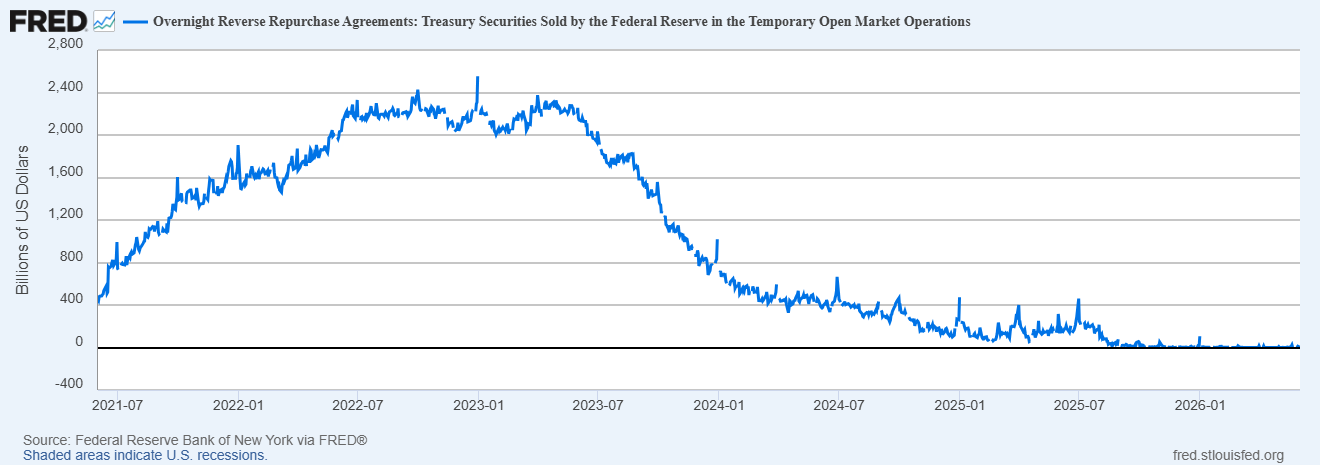

Recent research from the Federal Reserve Bank of New York demonstrates that Treasury issuance interacts directly with reserve balances and the overnight reverse repo facility, creating effects that extend far beyond conventional duration channels. This observation becomes especially important when considering the post-2022 period of quantitative tightening. A traditional portfolio-balance framework would predict substantial upward pressure on yields from the combination of increased Treasury issuance and Federal Reserve balance sheet reduction. Yet much of the adjustment occurred through declines in ON RRP balances rather than through large increases in term premiums.

Source: Federal Reserve Bank of St. Louis

Consequently, interpreting Treasury supply purely through convenience yields risks missing the monetary architecture in which these securities operate.

A second limitation of the ESM framework concerns international transmission. The paper implicitly assumes that Treasury spillovers reach Bund markets through relative pricing channels. Yet sovereign bond markets today are linked through common funding conditions as much as through investor substitution. For example, research from the ECB documents how dollar funding conditions increasingly influence euro-area bond markets through global collateral and repo channels. This implies that Bund-Treasury co-movement may reflect common funding constraints rather than merely substitution between safe assets.

Indeed, the distinction becomes particularly relevant when examining periods of elevated Treasury issuance. If additional Treasury supply expands the stock of collateral available to global funding markets, the resulting effects on Bund yields may arise through changes in repo conditions and dealer balance sheet utilization. Not through changes in investor demand for duration. This interpretation aligns more closely with the modern monetary system, where sovereign securities serve dual roles as investment assets and monetary instruments. The implication is that the concept of “specialness” itself may require reconsideration.

The ESM paper correctly identifies a changing relationship between Treasury supply and Bund yields. Yet the conclusion that Treasuries are becoming less special risks conflating changes in convenience premia with changes in monetary functionality. Treasuries remain the dominant collateral asset in global repo markets. They remain the primary reserve asset for central banks. They remain central to margining, derivatives clearing, and dollar funding. None of these functions has diminished materially. What has changed is the institutional environment in which Treasuries operate.