Do we really need another QE?

Since the pandemic-shock era, the US financial system has been operating with extraordinary levels of central-bank liquidity. The Fed’s large-scale asset purchases (its quantitative easing or QE programs), poured trillions of dollars into the system, effectively flooding many of the “pools, lakes and rivers” of money that underpin short-term funding markets. As the system moved into the period of quantitative tightening (QT) beginning in 2022, that liquidity was being drained. But recently we’ve seen renewed strains across money markets. Rates such as the Secured Overnight Financing Rate (SOFR) have spiked and repo rates have turned more volatile (I’ve discussed these dynamics in previous posts here or here, for those who haven’t followed). Naturally, the first “magic” solution that many commentators reach for is a restart of QE to calm things down. Readers of this blog know that I’ve long been a defender of QE, I see a legitimate role for it in times of distress, just as I see value in central banks maintaining an ample-reserves framework. But today, I’ll play the contrarian and argue that restarting QE now would be counterproductive. Instead, the Fed should adopt (or strengthen) its demand-driven central-banking framework (as I discussed here), sharpen its Standing Repo Facility (SRF) and other backstop tools, and focus on recognising the structural build-out of secured-funding markets and Treasury issuance as the root drivers, not simply the size of the balance sheet.

Now the question is: why restarting QE is the wrong answer? The intuitive argument for restarting QE is straightforward, inject more liquidity, lower short-term funding stress, calm SOFR and repo markets. Yet this fails (or could fail) on three levels.

First, QE is a blunt tool. It affects long-term rates and broad credit conditions, not the targeted plumbing of short-term secured markets. You don’t have QE for repos (or just for repos). As Fed Vice Chair Christopher Waller (and others) have argued, a mature ample-reserves regime and an operationally calibrated balance sheet can meet liquidity needs without returning to full QE-style duration expansion. QE also reverses the careful work of exiting massive expansions and introduces risks of maturity mismatch and longer-term distortions.

Second, the crisis-era dependence on ultra-large balance sheets has arguably embedded some fragility. When markets assume that the central bank will always expand the balance sheet at signs of stress, participants may increase leverage and reduce resilience. The repo markets have grown dramatically, some estimates place the US Treasury-collateralised repo market at near $12 trillion, with a significant portion bilateral and opaque. The moral hazard here is that a permanent expectation of backstop expansion invites risk accumulation and this may reduce incentives for market participants to self-insure or diversify.

Third, liquidity strains in the money markets are not simply a function of too few reserves. For example, the Fed’s balance sheet stands at roughly $6.5 trillion, while the current pace of balance sheet shrinkage is capped at $5 billion per month, far too small an amount to serve as a valid excuse. There is also a structural imbalance, namely the rapidly rising demand for secured funding (driven by large Treasury issuance and basis trades) alongside constrained supply (due to bank regulatory constraints, dealer capacity, rate arbitrage, you name it). For example, analysis shows that repo and Treasury market stress reflects supply-and-demand imbalances rather than purely central bank reserve exhaustion. Initiating QE would mask the underlying causes rather than resolving them.

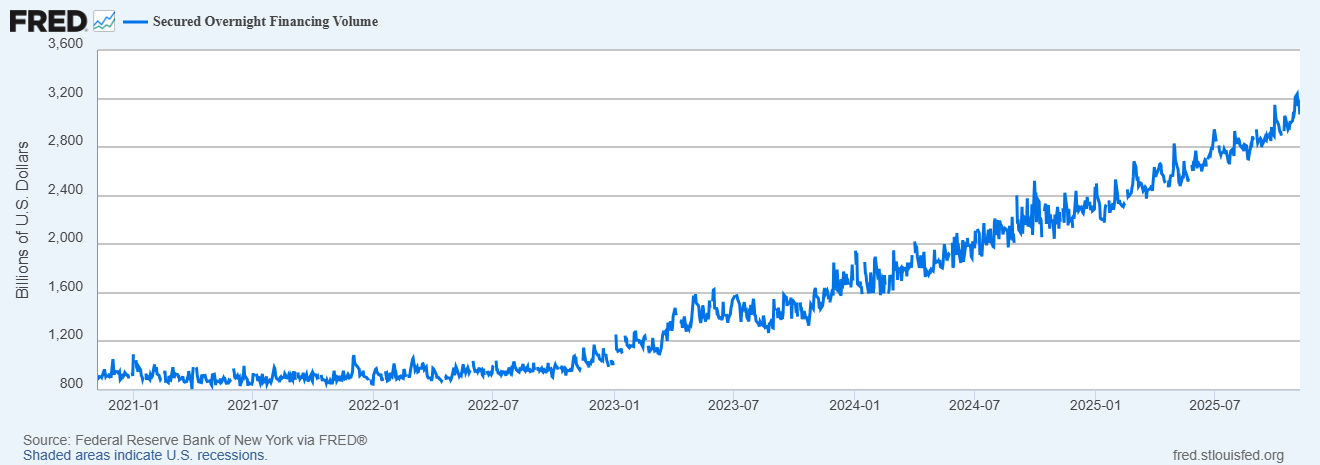

For me, and not just for me, a crucial driver of money-market volatility has been the US Treasury’s large scale of short-term issuance, as bill supply has surged to rebuild cash balances and meet deficit financing needs (as discussed here). That issuance drains liquidity from money markets (as cash flows into Treasury purchases and repo funding demand rises), thereby putting upward pressure on SOFR and repo spreads, especially since demand for repos will continue to grow with the growing fiscal deficit (as can also be seen in Secured Overnight Financing Volume; see the figure below). Meanwhile, short-term yields and repo rates have shown significant sensitivity to Treasury issuance events.

Source: Federal Reserve Bank of St. Louis

This suggests that liquidity stress in funding markets is embedded in the collateral flow and issuance structure of the government, not simply a central-bank liquidity shortage. The financial plumbing of the repo market depends critically on the supply of Treasury collateral and the ability of banks and dealers to intermediate secured funding. When collateral supply is abundant (and financing demand moderate) things are smooth. And of course, when issuance surges and settlement obligations spike (e.g., around coupons, taxes, or auctions) the system feels the strain.

And here we are (but not for long). As argued before, the US Treasury has been issuing record volumes of bills to rebuild its cash balance after the debt ceiling turmoil earlier this year. But the Treasury General Account (TGA) at the Fed is projected to return to its $850 billion target soon, after having been depleted during that standoff. Each dollar that flows into the TGA is a dollar drained from the banking system’s reserves. This is what has made the money markets feel “tight”. Now that the TGA is set to reach its target level, one of the main sources of tightness in money markets will fade away.

That distinction matters because the Fed’s role should not be to accommodate every temporary distortion in the fiscal plumbing with a permanent balance-sheet response. If the Treasury front-loads bill issuance, the resulting liquidity drawdown may feel painful, but it’s cyclical, not structural. To respond with QE, a tool designed for macroeconomic crises, not microstructural imbalances, would be to misdiagnose the problem entirely. The right response, from my point of view, lies in targeted, demand-driven liquidity support through the SRF, alongside increased engagement with hedge funds (to prevent an unwinding of the cash-futures basis trade) and a recomposition of the balance sheet with greater emphasis on short-term bills. This wouldn’t imply an actual expansion of the Fed’s balance sheet, I use the word recomposition intentionally, since these purchases would merely offset longer-duration bonds, as discussed here.

As such, rather than returning to broad QE, the Fed should elevate tools like the SRF. The SRF was created to provide overnight liquidity in exchange for eligible collateral like Treasuries, effectively acting as a safety valve in money-market stress. Recent usage, while not at crisis levels, has shown that participants turn to it when short-term stresses flare up. The problem is not that the Fed lacks tools, but that it has been too hesitant to use them aggressively. Strengthening and normalizing the SRF as an everyday stabilizer, rather than treating it as a crisis lever, would allow the Fed to manage volatility without reigniting the expectations of perpetual QE. But as I discussed in this post, the SRF’s current design limits its effectiveness. It has a daily cap of $500 billion across two auctions, whereas a true demand-driven system would meet all eligible liquidity demand at the policy rate. On stress days, the cap could fall short, undermining its credibility as a reliable backstop. Access is also limited to primary dealers and depository institutions. Expanding it to hedge funds or money market funds could improve effectiveness, especially given their central role in Treasury markets and the risks posed by cash-futures basis unwinds. Moral hazard is a concern, but so is excluding key liquidity providers from central-bank support.

Finally, the SRF only accepts top-tier collateral, such as Treasuries, agency debt, and agency MBS, limiting flexibility compared with the discount window. In acute stress, firms may need to pledge less liquid assets. This suggests a potential case for a facility akin to the post-2008 TSLF, allowing broader collateral to be swapped for high-quality securities.

A demand-driven framework implies that the central bank supplies reserves in response to genuine market need, not in anticipation of it. This is the opposite of the QE logic. QE was supply-driven, with the Fed deciding how much liquidity to inject based on macroeconomic targets. A demand-driven approach accepts that liquidity demand fluctuates with the structure of the market itself, with Treasury issuance or with dealer balance-sheet constraints, and builds a flexible operational regime around those dynamics. As Lorie Logan, President of the Dallas Fed, recently argued, the Fed’s portfolio composition matters more than its absolute size. Holding more short-term securities like Treasury bills provides the Fed with agility. It allows reserves to ebb and flow naturally, maintaining control of short-term rates without constant resort to new asset-purchase programs.

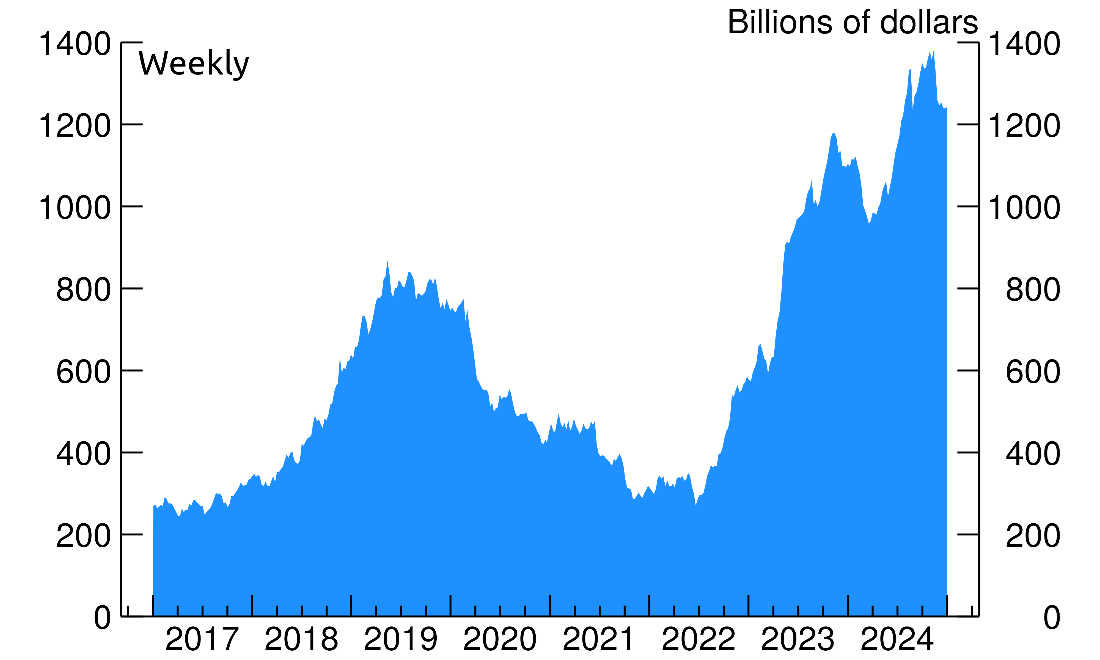

Of course, volatility in money markets makes policymakers nervous, and for good reason. SOFR is now the anchor of the post-LIBOR world. It prices trillions in derivatives, loans, and securities. When it moves sharply, it transmits stress throughout the financial system. But it’s important to recognize that some of that volatility originates not from reserve scarcity but from the leveraged strategies built around Treasury markets themselves. Hedge funds engaging in basis trades, buying cash Treasuries and shorting Treasury futures, rely heavily on repo financing (you can read more about this here). For example, the figure below shows leveraged funds’ short positions in Treasury futures.

Source: Federal Reserve Notes

When repo rates spike, their funding costs surge, and positions can unwind violently, something that happened in April 2025, as I discussed in detail here. This interdependence between Treasury issuance and leveraged positioning is what makes SOFR volatility appear more ominous than it really is. But even in this scenario, the Federal Reserve does not need to restart QE. As argued in a paper by Kashyap et al. (2025), it is sufficient for the Fed to engage in Treasury purchases while simultaneously selling Treasury futures. These transactions would directly offset the positions that hedge funds are compelled to unwind, relieving market stress immediately without altering the stance of monetary policy or materially affecting term premia1. Crucially, the authors suggest that these operations be conducted through auctions at a discount that penalizes participants. This design prevents market actors from expecting full loss protection, thereby mitigating moral hazard. Because the hedged purchases explicitly avoid taking on duration risk, unlike traditional QE, this method diminishes the incentive for excessive risk-taking and limits the likelihood of Fed-induced moral hazard.

These measures can be implemented without restarting QE. It is argued that restarting QE could blunt the market’s price signals. For example, if repo rates spike and the Fed simply intervenes by buying long-dated assets, participants may assume the central bank will always cushion short-term funding issues, creating a moral hazard. Moreover, QE acts on longer-term rates and credit markets, not precisely tuned to repo/secured-funding frictions. It may also distort yield curves and compress risk-premia. Some Fed officials have warned about these trade-offs: Waller pointed out that QE introduces maturity-mismatch and extends the central bank’s interest-rate-risk exposure.

More than that, the instinct to restart QE is more about market psychology, a belief that the Fed’s balance sheet can fix any instability. But that mindset is precisely what creates structural fragility. If every period of funding stress (so not crises) is met with another wave of central-bank asset purchases, the market never rebuilds its own liquidity buffers. The risk is we can end up with a central bank that cannot shrink without breaking the plumbing it once held together, the same problem that began after 2008 and deepened during Covid-19 crisis.

In more detail, the Fed, instead of directly intervening through QE-style purchases that increase its balance sheet and duration exposure, could step in as a counterparty to this unwind. It would buy the Treasury securities that hedge funds are selling, supporting their prices and liquidity. At the same time, the Fed would sell an equivalent amount of Treasury futures to hedge the market risk it’s taking on. Effectively, this neutralizes the risk to the Fed’s balance sheet and term premia while stabilizing the short-term funding markets.