Prime-broker centric environment

Prime brokerage services stand as a cornerstone for hedge funds, providing access to leverage, market infrastructure, clearing, and custody - all critical for funds aiming to amplify returns and diversify strategies. While prime brokers (PBs) are traditionally viewed as low-risk providers, recent episodes and data suggest that the relationship between hedge funds and PBs is a two-way street with significant systemic implications.

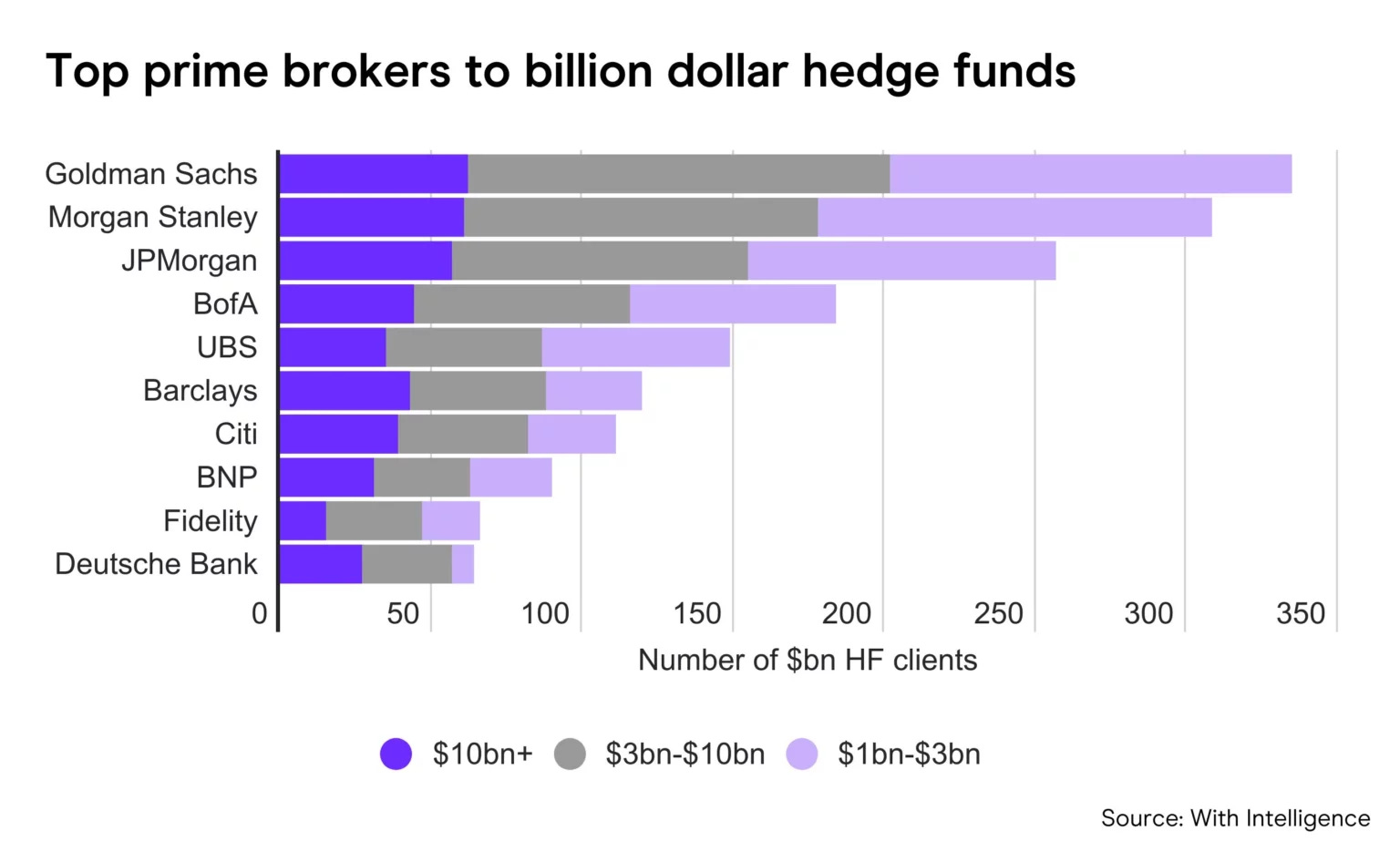

As of end-2022, US-registered hedge funds managed over $4.5 trillion in gross assets, largely funded through prime brokerage arrangements with global systemically important banks. The scale of leverage and opacity inherent in many hedge fund positions creates vulnerabilities for both sides. This is also called the wrong-way risk (WWR), where the opaqueness of funds' positions can create vulnerabilities for PBs in times of distress. This dynamic was vividly illustrated in the Archegos Capital Management collapse, where concentrated, leveraged bets went largely unnoticed by PBs due to opaqueness and insufficient risk management, ultimately causing severe losses for involved banks like Credit Suisse. Below we can see the main 10 prime brokers to (billion dollar) hedge funds.

Source: Withintelligence

More broadly, hedge funds’ procyclical leverage behaviors - taking on more margin loans when markets rise and facing tighter conditions during stress - create an unstable feedback loop. Prime brokers tend to relax lending terms in buoyant markets to accommodate hedge funds’ demand, only to enforce strict margin calls when volatility spikes. This pattern amplifies market swings as forced selling from margin calls depresses prices further, which in turn triggers additional calls.

In early April 2025, this dynamic reemerged with intensity. In response to President Trump’s tariff announcements and ensuing global market instability, major banks issued the largest margin calls since the pandemic onset in 2020. This broad-based selling spanned sectors from technology to consumer goods and even safe havens like gold, which dropped over 3% as investors liquidated positions to meet margin requirements.

One prime brokerage executive summarized the episode as a convergence of sharp declines in rates, equities, and oil, triggering widespread margin calls. On Wall Street, prime brokerage teams convened emergency meetings to assess risk exposure and client liquidity, emphasizing proactive engagement to mitigate systemic fallout. Morgan Stanley’s prime brokerage report highlighted that US-based long/short equity funds suffered their worst performance since 2016, with average losses of 2.6% in a single day and net leverage falling to an 18-month low of roughly 42%.

In more detail, OSTTRA, which operates a platform reconciling more than 90% of bilateral derivatives globally, reported a staggering 180% increase in total margin call value from April 2 to 10, signaling acute liquidity stress on investors. The demand for margin calls rose 35%, much driven by variation margin, additional collateral investors must post to reflect fluctuating market values and prevent default. OSTTRA’s data showed that disputes between trading parties surged by 25%, highlighting the friction and operational strain during periods of heightened volatility.

To contextualize this pressure, OSTTRA illustrated that a hedge fund managing 100 margin calls per day at an average of $5 million per call - normally responsible for $500 million in daily collateral flows - faced an abrupt increase of $900 million in additional collateral demands during the turmoil. This pushed its total daily margin obligations to $1.4 billion, a large portion of which likely required cash funding amid already stressed liquidity conditions.

This margin call pressure was pervasive across asset classes, including equities, rates, foreign exchange, commodities, credit derivatives, and repurchase agreements, reflecting the systemic reach of prime brokerage–hedge fund interactions and the broad market implications of their deleveraging.

The scale and speed of deleveraging resembled patterns seen during the 2020 COVID sell-off and the 2023 US regional bank crisis. These events reveal how hedge funds and their prime brokers act as a nexus where market stress can quickly transmit and escalate, highlighting the critical importance of dynamic risk management and international supervisory coordination.

However, beyond the margin calls and leverage cycles, these events also highlight a more fundamental transformation in the domestic financial market structure: the rise of prime brokerage firms as dominant intermediaries and the corresponding erosion of traditional dealer-centric liquidity provision.

Unlike dealing banks, which use their balance sheets to absorb trades and provide market-making liquidity, prime brokers operate largely as intermediaries that direct order flows from one institution to another for a fee without taking on inventory risk themselves. In other words, their business model centers on facilitating trade flows and charging fees rather than stabilizing markets through balance sheet intermediation. That's why, just two days ago, I discussed how complex the financial system has become with its increasing ‘hedge-ification’.

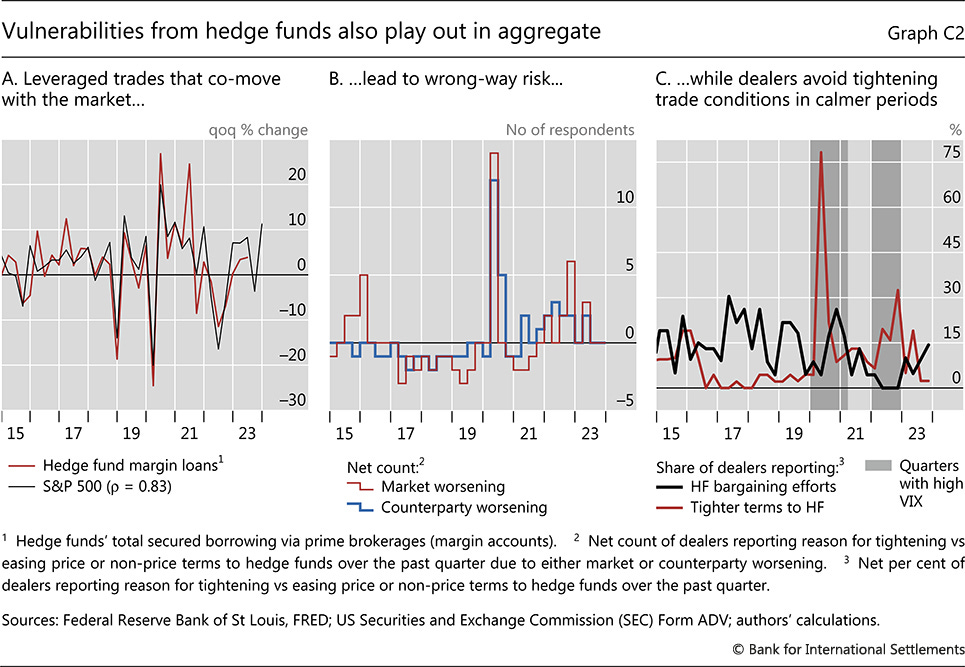

This shift has significant implications for market liquidity and fragility. When hedge funds face margin calls and must rapidly liquidate positions, prime brokers do not act as shock absorbers. Instead, they pass trades downstream, exacerbating selling pressure and market volatility. The liquidity that was once buffered by dealer banks’ willingness to carry positions has thinned, replaced by a broker-centric system that is more vulnerable to rapid deleveraging spirals. And this vulnerability plays out in aggregate…

Source: Bank of International Settlements

The April 2025 turmoil exemplifies how this broker-based market structure intensifies instability. As such, in this synthetic, broker-centric environment, the ability of regulators and central banks to manage liquidity crises is constrained. Prime brokers, by not internalizing risk on their balance sheets, reduce the buffer capacity of the financial system and amplify the procyclical dynamics of leverage and margining. The concentration of hedge fund borrowing within a small number of PBs further concentrates systemic risk, as any shock can quickly cascade through interconnected exposures.