US Treasury buybacks and the market plumbing

On June 3, 2025, an event took place that arguably deserved more public attention - not because of its scale, but because of the motivations behind it.

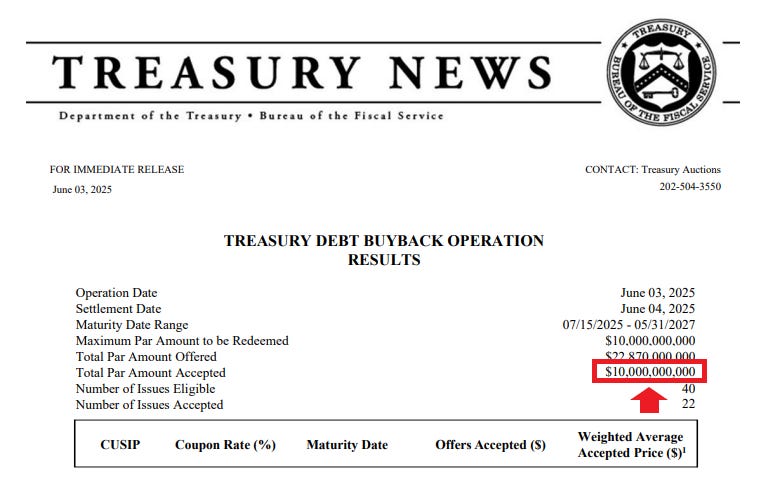

What was that event? Well, the US Treasury conducted its largest-ever buyback operation, repurchasing $10 billion in outstanding government debt. The market offered over twice that amount in bids - $22.87 billion - highlighting pent-up demand for this kind of liquidity operation. While the headline number pales in comparison to the $36.5 trillion federal debt load, the implications of this move go far beyond nominal debt management. What’s at stake is a deep structural issue in dollar markets: the scarcity of usable collateral, particularly on-the-run (OTR) Treasuries.

Source: Barchart

At first glance, buybacks may seem like a throwback to the brief window between 2000 and 2002, when the US used budget surpluses to modestly retire long-dated debt. For instance, through this program, the US Treasury used $67.5 billion in 45 separate buyback operations. But the current context is profoundly different. These aren’t surplus-driven redemptions. Instead, Treasury Secretary Scott Bessent is reintroducing buybacks as a form of liquidity enhancement - part of a $30 billion quarterly effort - to address distortions in the Treasury curve and mitigate (potential) disruptions in repo, funding markets and basis trades.

To understand the mechanics, it’s essential to differentiate between on-the-run and off-the-run (OFR) securities. OTR Treasuries are the most recently issued notes and bonds. They are the most liquid, most actively traded, and the most useful in financial plumbing, whether as repo collateral, hedging instruments, or benchmarks in futures markets. Their liquidity and tight bid-ask spreads make them invaluable in a world where funding efficiency is paramount.

OFR Treasuries, by contrast, tend to decay into obscurity. They’re often held to maturity in insurance reserves, pension portfolios, or sovereign wealth funds. Many trade at steep discounts due to low coupons and longer durations, making them unattractive for collateral transformation or short-term funding purposes (and most of the time, these institutions are unwilling to lend them into repos). Despite being legally equivalent in credit risk, they are functionally inferior from a monetary operations perspective.

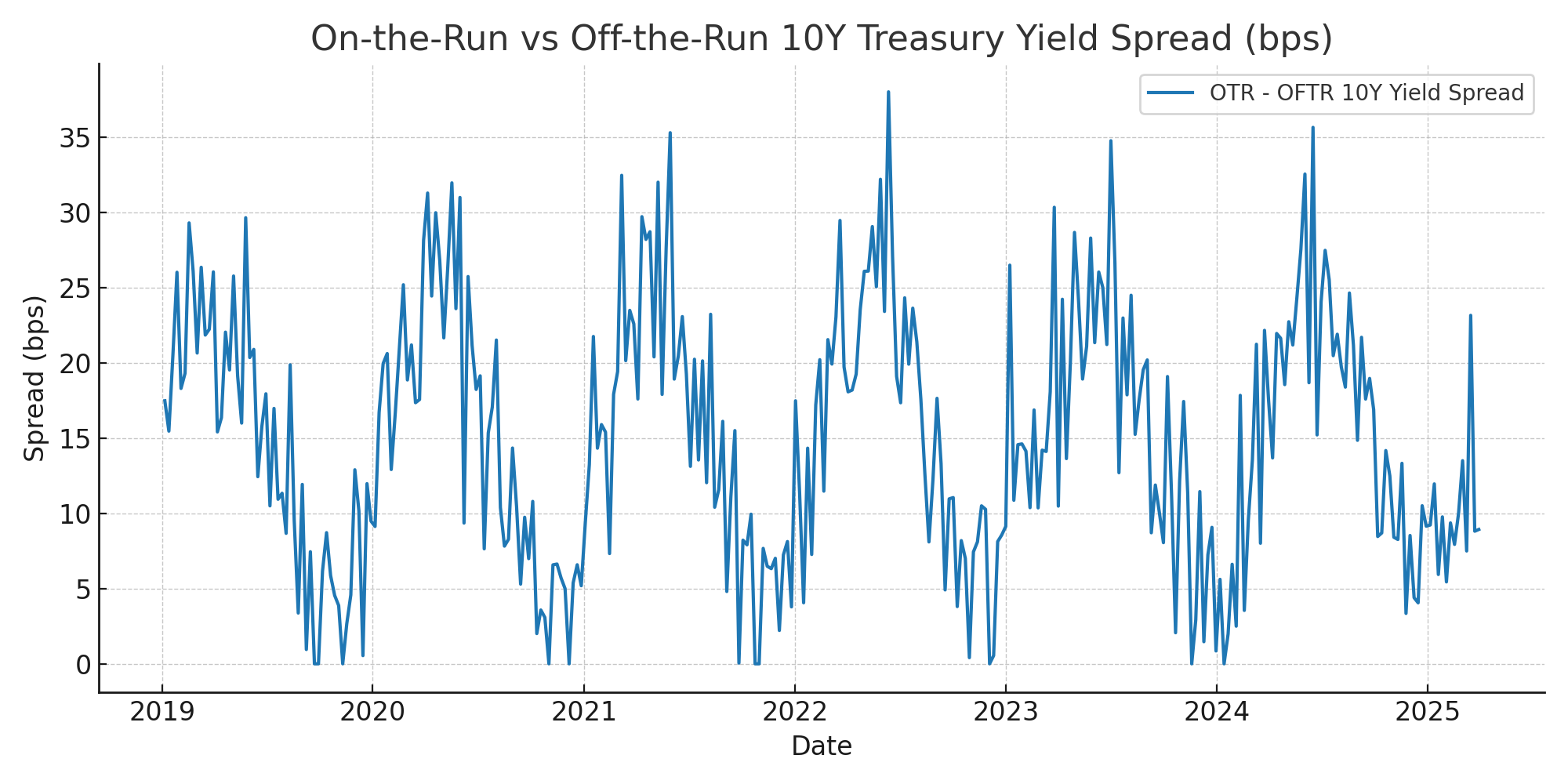

In recent months, the yield spread between these two asset classes has widened, a pattern typically seen during periods of market stress, while the spread tends to narrow under more stable conditions. This context helps clarify the dynamics illustrated in the chart above. Turbulence in the basis trade - where hedge funds arbitrage small differences between cash and futures prices - has made illiquid Treasuries especially volatile. Events like the pandemic crisis, the dollar liquidity squeeze of December 2024 or the basis unwind of April 2025 exposed a critical vulnerability: when stress hits, markets flock to OTRs, while OFRs become toxic. Dealers, unable to offload them easily, face balance sheet strain (also because of the supplementary leverage ratio, we already discussed it here or here). Central banks and reserve managers - especially from abroad - are often forced sellers of OFRs, exacerbating illiquidity. I recall that Darrell Duffie argued that off-the-run Treasuries were at the epicenter of the pandemic crisis. This happened, in his words, because “the biggest sellers were those that had set them aside for a rainy day, and that day arrived when the World Health Organization announced a COVID pandemic.” End of quote.

So, the Treasury’s buyback strategy can thus be seen as a subtle intervention into this fragility. By using proceeds from short-term bill issuance - assets in high demand - to purchase illiquid OFRs, the Treasury is effectively rotating the composition of its outstanding debt toward more usable instruments. This isn’t stealth quantitative easing or stealth QE (a label frequently applied to both the US Treasury and the Federal Reserve over the years). Put simply, stealth QE refers to financial operations that are small in volume but are argued to have outsized effects on certain interest rates or market segments. In other words, it's often used to “assist” financial institutions through injections of liquidity that don’t require broad public debate or formal announcements. But as I mentioned earlier, that’s not what’s happening here. The scale is too small to materially affect long-term yields, and monetary policy remains firmly in the Fed’s domain. Rather, it is a monetary infrastructure adjustment, aimed at realigning the supply of securities with the demand structure of modern collateral markets.

There’s also a duration management angle. Without buybacks, surpluses or rollovers tend to target the front-end of the curve, leading to a gradual increase in the average maturity of Treasury debt. That can become costly when long-term yields rise, as they have recently. Buybacks allow the Treasury to issue more short-term bills and repurchase longer-dated, higher-coupon bonds, slightly reducing debt-servicing costs while improving liquidity conditions.

Crucially, this isn’t about reducing the federal debt. The scale is too limited. Instead, it reflects an acknowledgment that not all Treasuries are created equal. Of the $36.5 trillion outstanding, only a narrow band of securities function as high-quality, liquid assets (HQLA) in funding markets. The rest are, in effect, monetary deadweight.

By reactivating buybacks and targeting the replacement of OFRs with new, liquid OTRs, the Treasury is operating more like a financial utility provider than a mere debt manager. In doing so, it signals a deeper truth, that the US sovereign debt market is the backbone of global dollar liquidity. And that liquidity depends not just on how much debt is issued, but what kind.

Great explanation Alex