Why EU Bonds Still Can’t Replace US Treasuries - No Matter How Big the Dream

For decades, US Treasuries have been the bedrock of the global financial system - deep, liquid, and backed by the full faith and credit of the world’s most powerful economy. They anchor everything from global reserves to repo markets and cross-border derivatives. But in today’s fracturing geopolitical context, some are asking whether the dollar’s dominance - and with it, the reign of Treasuries - might be slowly eroding. And for many, 9th of April spike in US Treasury yields marked the moment when the funeral bells began tolling for the US-centric financial architecture (I already offered a counterargument, spoiler alert, USTs are not dead).

In this context, Europe is starting to imagine bigger things for the euro.

The idea is simple: in a world where US Treasuries are no longer seen as politically or financially risk-free, Euro-denominated bonds could emerge as a credible alternative. At least in theory.

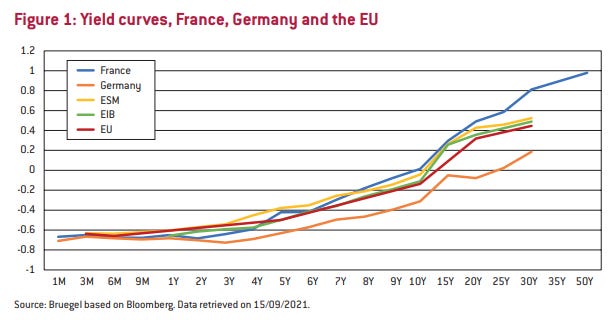

The European Union has taken real steps in this direction. The launch of the NextGenerationEU (NGEU) program during the COVID-19 crisis was a watershed moment. For the first time, the European Commission was empowered to borrow at scale on behalf of all member states. In more detail, it was the first time the European Commission adopted a large-scale unified approach - taking on debt directly through bond issuance, with the resulting funds redistributed to member states. This significantly lowered borrowing costs, as the Commission is seen as a far safer borrower than any individual member state. Since then, nearly €600 billion in bonds have been issued under this framework, and investor demand has been strong. On average, EU bonds have been oversubscribed more than eightfold, and yields remain lower than those of many member states.

Source: Bruegel

This success has led some to wonder: could EU bonds become the euro area’s version of US Treasuries? Could they serve as the long-elusive euro safe asset - the missing cornerstone of an international euro system?

At first glance, the timing seems ripe. The war in Ukraine, Europe’s accelerating green transition, and the push for greater defense autonomy have all revived the idea of collective European spending. Calls for new rounds of common debt issuance are growing louder - from “RePowerEU” to proposals for a “ReArm Europe” initiative. Europe’s leaders are beginning to speak the language of shared industrial policy and fiscal solidarity.

But here’s the catch: the foundation for this ambition remains politically and structurally fragile.

The NGEU program, for all its success, is explicitly temporary. The debt is scheduled to be fully repaid by 2058, and its legal justification was built on the premise of a one-off crisis response. There is currently no standing authority - and more importantly, no long-term political consensus - to make EU borrowing permanent. Unless that changes, euro-denominated bonds will remain a patchwork of emergency instruments, not the kind of enduring, predictable safe asset that global investors require. “Funny” story - as part of my PhD research, which focuses on the euro area’s primary dealer system (a system that emerged directly as a result of NGEU), I had conversations with members of the European Commission. Their response was unanimous and clear: the NGEU cannot become a permanent fixture. Making it so would require a fundamental overhaul of the current European treaties.

That is why, some have proposed rolling over NGEU debt, issuing new tranches under existing frameworks, or even consolidating various EU-level borrowings into a more coherent structure. But these workarounds don’t resolve the deeper issue: permanence and credibility. The global demand for safe assets isn’t just about quantity or yield. It’s about confidence - the belief that, in times of crisis, the issuer has both the political and fiscal capacity to backstop the system. In the absence of a permanent fiscal capacity at the EU level, you inevitably have to rely on the member states.

And that’s where Europe runs into its hardest constraint: Germany.

Any move toward permanent Eurobonds - real benchmark securities backed by collective EU credit - would require Berlin’s full endorsement and fiscal participation. There is no alternative. Germany remains the eurozone’s largest economy, its most creditworthy issuer, and the linchpin of its financial architecture. Without German backing, any attempt at fiscal union is a house without a foundation.

But Germany’s political culture is deeply rooted in fiscal conservatism. The constitutional debt brake (although it has undergone recent modifications), the rulings of the Federal Constitutional Court, and decades of political discourse have entrenched a belief that joint liabilities are a slippery slope. Berlin may tolerate temporary exceptions, as it did with the NGEU and might again with defense-related spending. But transforming those exceptions into permanent architecture is a different matter entirely.

There have also been proposals to extend euro swap lines to third countries, especially to free trade partners such as Mercosur, particularly now that a deeper free trade agreement between the EU and Mercosur is established. Thus, free trade partners would have easy access to the euro, which could increase the use of this currency in this free trade relationship. There has even been consensus on launching futures instruments for EU bonds on Eurex, which are set to be introduced in September 2025. Moreover, the European Commission created a dedicated EU Repo Facility for the primary dealers under the NGEU framework (why this wasn’t handled through the ECB’s repo operations - especially given that all primary dealers are already deposit-taking institutions with access to the ECB’s balance sheet - remains unclear to me). However, these initiatives do not fundamentally change the underlying structural issues. For instance, extending euro swap lines to external partners is a diplomatic and technical gesture - useful, but limited. It doesn't address the structural weaknesses discussed earlier (like the lack of a permanent EU bond or fiscal authority).

This is the paradox at the heart of the euro’s internationalization effort. Europe wants to play a larger role in global finance. It wants to promote the euro as a currency of stability, autonomy, and influence. But it is unwilling - or politically unable - to build the institutions that such a role requires.

A truly global euro would need a permanent, unified fiscal anchor, a European Treasury with the capacity to issue debt at scale, backed by a coherent political mandate. Anything less remains a workaround.

Yes, US Treasuries have problems. Yes, their political underpinnings are shakier than they once were. But they remain unmatched in size, liquidity, and - crucially - permanence. And so long as the EU continues to rely on temporary programs, ad hoc instruments, and politically contested fiscal schemes, Euro-denominated bonds will not replace US Treasuries.

At most, they will offer a complementary store of value, a regional alternative for reserve diversification, not a global benchmark.

So the question isn’t whether the euro can rise as the dollar stumbles. It’s whether Europe is willing to do the institutional heavy lifting - to turn emergency fiscal improvisation into lasting fiscal union.

Until then, Eurobonds will remain what they are today: instruments of crisis management - not instruments of leadership.