Why Double-Pledging Is Back and Why It Matters

The current resurgence of double pledging practices across parts of the credit system represents (or could become) a structural vulnerability. To make things interesting, it has re-emerged at the intersection of private credit, subprime auto finance, and opaque funding structures (where interesting things always happen). While the practice itself is hardly new (it is argued that the first recorded court dispute of a double pledge dates back to Ancient Greece), its reappearance at this stage of the credit cycle, combined with the size and complexity of the contemporary private credit market, suggests that what might once have been dismissed as a series of isolated frauds is now symptomatic of deeper systemic (let’s call it) weaknesses.

In its essence, double pledging is the use of the same underlying asset (whether a loan, an invoice, or a title) as collateral for multiple credit facilities. It is a deceptively simple mechanism, but one with the capacity to undermine the very logic of secured lending. What makes this issue particularly dangerous is that its effects remain largely invisible until a borrower defaults, at which point multiple lenders discover that they were never secured in the way they believed.

The phenomenon itself is not an abstract legal or technical matter. There are operational, infrastructural, and ultimately systemic implications. As you probably know, secured lending depends on three interlocking assumptions: that the collateral exists, that it is unique, and that its ownership is clear and enforceable. Double pledging shatters all three simultaneously. When this happens in a sufficiently large or interconnected market, the problem is not limited to a single borrower or creditor but extends to the entire edifice of secured financing. In a nutshell, what was considered overcollateralized can quickly turn out to be underfunded (which means uncertainty). And in credit markets, uncertainty propagates through confidence channels and valuation metrics. This is precisely why recent cases involving First Brands Group (about First Brands I already discussed here) and Tricolor Holdings deserve to be read as signals of latent structural fragility related to double pledged collateral.

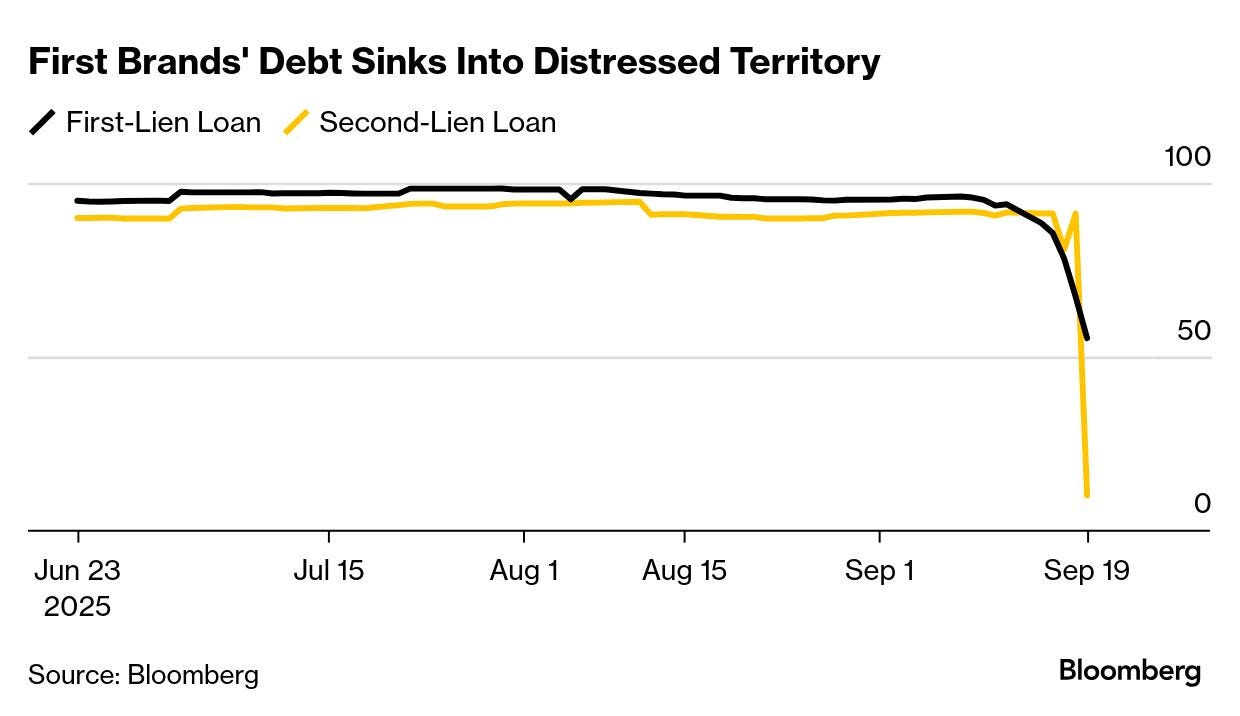

In the case of First Brands, the issues emerged around the factoring of receivables (among others!). Briefly, this is a financing practice in which a company sells its outstanding invoices (accounts receivable) to a lender or specialized financing firm (called a factor) at a discount in exchange for immediate cash. This allows the company to unlock liquidity before the customer actually pays. This a practice long considered routine, stable, and, in some circles, almost riskless. First Brands, with liabilities exceeding $10 billion (firm’s bankruptcy filing now estimates liabilities up to $50 billion, much of the previously unknown debt appearing tied to off-balance sheet loans backed by asset), had for years relied on factoring to unlock liquidity from its operations. In principle, this is a legitimate and efficient liquidity management strategy. However, the entire structure depends on a crucial assumption: that each receivable is sold once, to a single lender, and that the claim on the asset is exclusive. When filings revealed extensive commingling of collateral across multiple credit lines, the assumption of exclusivity collapsed. What was supposed to be a straightforward transaction between a borrower and a single lender turned out to be layered with multiple claims on the same underlying asset. Factoring lenders, who typically advance capital under the belief that their claim is senior and uncontested, suddenly found themselves in competition with one another. In this environment, legal recourse may clarify ownership after months or years, but by then the liquidity event has already occurred and the damage to market confidence is irreversible. As a consequence, First Brands’ debt plummeted in the past few weeks, as can be seen in the figure below.

Source: Bloomberg

The situation involving Tricolor Holdings exposed an even more direct and quantifiable manifestation of the problem. As a major player in subprime auto lending with a large borrower base and significant warehouse credit lines extended by institutions such as JPMorgan Chase, Fifth Third Bancorp, and Barclays, Tricolor’s financial structure relied on the routine pledging of loan portfolios as collateral for these facilities. Briefly, warehouse credit lines are essentially short-term funding pipelines that allow lenders like Tricolor Holdings to keep issuing loans without waiting for repayment. For example, when the company originates auto loans, those loans are bundled into portfolios and pledged as collateral to banks such as JPMorgan Chase, Fifth Third Bancorp, and Barclays. In return, the banks provide warehouse credit lines, which are revolving credit facilities that advance cash against the value of those pledged loans. This structure lets originators finance new lending while waiting to securitize or refinance the loans later on.

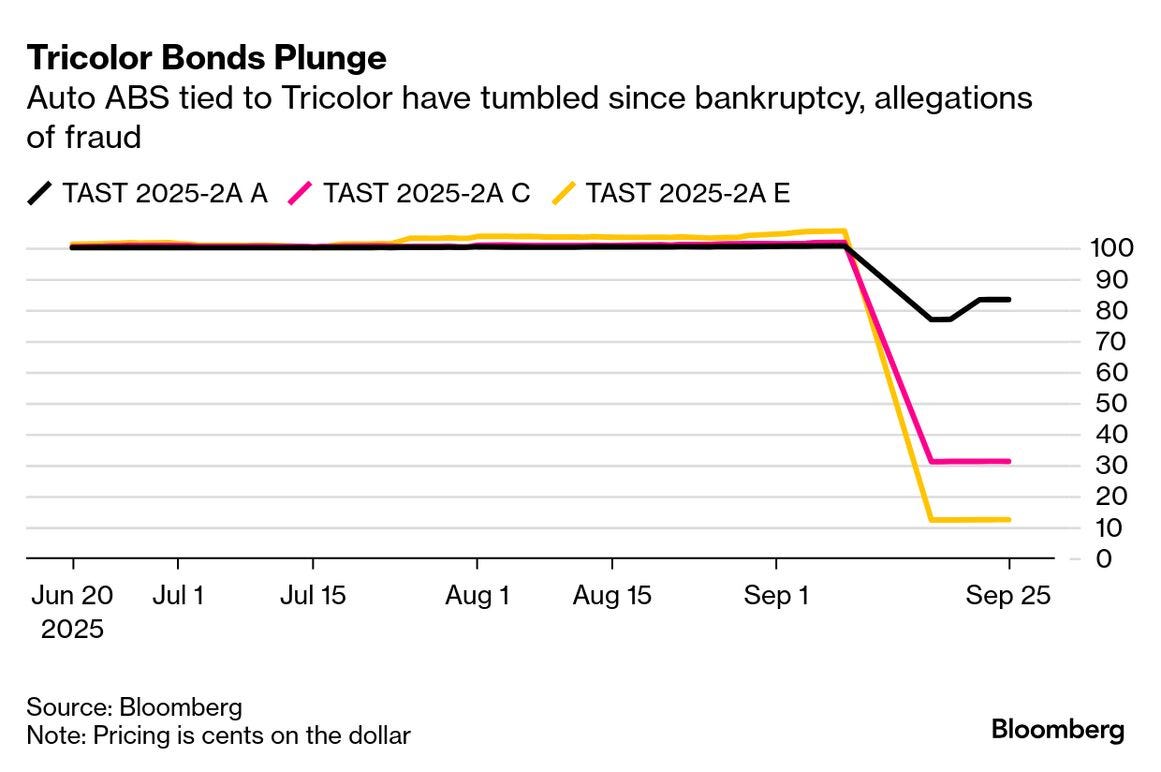

And so, when the company entered into liquidation proceedings, it was revealed that roughly 40 percent of its pledged loan pool (the loan pool was close to 70,000 active loans) may have been duplicated across multiple lenders. Moreover, at least 29,000 loans pledged to creditors were tied to vehicles already securing other debts. Identical vehicle identification numbers appeared in different collateral pools. The discovery was not the result of routine oversight mechanisms, but of a collapse that forced lenders to reconcile their exposures in real time. In the aftermath, some asset-backed securities (ABS) tied to Tricolor’s loan portfolios traded as low as 12 cents on the dollar (as can be seen in the figure below). The unsecured reality of what lenders had believed to be secured claims triggered rapid repricing (write-downs) and a reassessment of warehouse credit practices across the sector.

Source: Bloomberg

The mechanics of double pledging are conceptually straightforward (but institutionally corrosive, if I may). In a functioning secured lending system, the pledge of collateral establishes an exclusive security interest for a specific creditor. That exclusivity allows the creditor to assess its risk exposure and of course enforce its claims in the event of borrower default. Double pledging replaces exclusivity with ambiguity. Multiple creditors may simultaneously hold what they believe to be valid and senior claims over the same asset. The moment these claims are tested in default or liquidation, the structure reveals itself to be built on conflicting legal representations. This is dangerous because misrepresentation of collateral quickly transforms into a broader funding shock. As a consequence, lenders, confronted with losses they did not anticipate (as it is the case with JPMorgan or Barclays and their loans to Tricolor), tighten collateral verification standards. In that moment, funding becomes scarcer, more expensive and haircuts rise. And in a market environment that relies on continuous refinancing, this dynamic can set off a destabilizing spiral (think of a negative feedback loop).

This spiral is amplified by the nature of today’s private credit markets. Much of the credit intermediation outside the traditional banking system now takes place in some opaque structures with minimal standardization. Unlike public securitizations, which are subject to trustee oversight and at least some degree of market transparency, private credit facilities often operate on bilateral agreements or lightly syndicated arrangements (I discussed about this opacity in private credit markets here, here and especially here). This structural opacity makes double pledging more difficult to detect in real time and allows problems to build up quietly. When lenders rely on borrower self-reporting or sample-based verification of collateral pools, it becomes entirely possible for an asset to be pledged twice (or even more than that, see again Tricolor and its 29,000 loans pledged to creditors that were tied to vehicles already securing other debts) without triggering immediate alarms. That arrangement may work for years under stable conditions, but as soon as liquidity tightens or borrower credit quality weakens… Well, let’s say things tend to become “interesting”.

The dynamics have uncomfortable historical parallels. In the years preceding the GFC of 2007–2009, the securitization and repo markets operated on the presumption that collateral quality was both transparent and reliable. Documentation, custodial oversight, and representations were assumed to be sound. When defaults began to rise, it became clear that many of these assumptions were illusory (mostly related to private-label generated collateral). Mortgage cash flows had been tranched and sold multiple times with overlapping claims, documentation was incomplete, and what investors thought they owned could not be cleanly enforced (also, do you remember Lehman Brother’s Repo 105 maneuver back in the days?). The collapse of confidence in collateral quality (rather than the absolute level of credit losses) was the key accelerant of the funding freeze. As a result, trust in the plumbing of secured finance evaporated. It is not difficult to see how a similar dynamic could re-emerge if double pledging in the private credit and auto lending ecosystem becomes more widespread. I’m not saying we are there yet, but you never know. Especially since the progression from individual cases of double pledging to systemic funding stress follows a well-established pattern. Once a major borrower is revealed to have pledged assets multiple times, lenders across the sector reassess their exposure and tighten collateral verification procedures. This in turn reduces the effective availability of credit, raises the cost of financing, and shortens maturities. Borrowers that were not engaged in fraudulent practices but that operate on thin liquidity margins find it more difficult to roll their credit lines. The resulting distress spreads beyond the initial bad actors, affecting the entire funding ecosystem. Asset prices decline as investors demand higher risk premia. And so, a problem that initially appeared idiosyncratic becomes systemic through the mechanism of collective doubt.

The response from lenders and market participants to date has been reactive rather than preventive. Legal covenants, representations, and warranties are used as ex-post mechanisms to address breaches. Litigation and recovery actions may allow lenders to recoup some losses, but they do little to prevent the funding dislocations that occur immediately after the revelation of fraud. What the market currently lacks is a robust, standardized infrastructure for verifying collateral in real time. This is not a technological impossibility. Real-time collateral registries, whether centralized or distributed, could make it effectively impossible to pledge the same asset twice. VIN-level tracking systems integrated directly into warehouse lending facilities would allow lenders to confirm collateral exclusivity before advancing funds (more about all this here). For receivables financing, blockchain-based registries capable of recording unique identifiers and transfers already exist in pilot form. Yet widespread adoption has been slow, largely because the opacity of existing practices serves the commercial interests of both borrowers and some lenders during periods of expansion.

The underlying structural weakness is also rooted in infrastructural fragmentation. Ownership records for many forms of collateral, such as auto titles, receivables, or loan pools, are neither centralized nor technologically robust. In many cases, collateral is tracked through spreadsheets, PDFs, email attachments, or borrower-maintained databases, with no authoritative ledger that establishes uniqueness of claim. Auto titles, in particular, remain heavily dependent on state-level registries, often involving paper records or systems not designed for real-time financial tracking. This creates an environment in which multiple lenders can be presented with what appear to be legitimate “originals” of the same asset. Detecting these inconsistencies requires granular, real-time monitoring across counterparties, something that very few lenders currently implement systematically.

A shift from post hoc enforcement to proactive verification is ultimately the only way to address the structural vulnerability (at least in my modest opinion). Reliance on borrower representations and statistical sampling may have been sufficient in an era of low rates and abundant liquidity, but it is inadequate in a more stressed credit environment. Automated verification systems that cross-check identifiers across facilities and detect duplicates in real time would significantly reduce the opportunity for double pledging. This would need to be complemented by regulatory measures aimed at increasing disclosure and standardization in private credit markets. A targeted regulatory perimeter that does not seek to fully replicate bank-style supervision but that mandates minimum verification standards for collateral could go a long way toward preventing systemic “abuse” (tough word, I know).

Anyway, the post is already too long and it needs a conclusion. The central takeaway is that the resurgence of double pledging at this stage of the credit cycle should not be dismissed as mere coincidence. The conditions that make such practices attractive are precisely those that tend to precede broader credit stress events. The cases of Tricolor and First Brands may ultimately be resolved through legal proceedings, recoveries, and isolated write-downs. But the more important question is whether they are the first signs of a structural fissure. If lenders respond by materially increasing haircuts on warehouse lines, slowing new lending to opaque originators, and widening spreads on ABSs, this would signal that market confidence in the uniqueness and enforceability of collateral is eroding. And when confidence in collateral weakens, the effects are never confined to the immediate market segment where the problem originates.